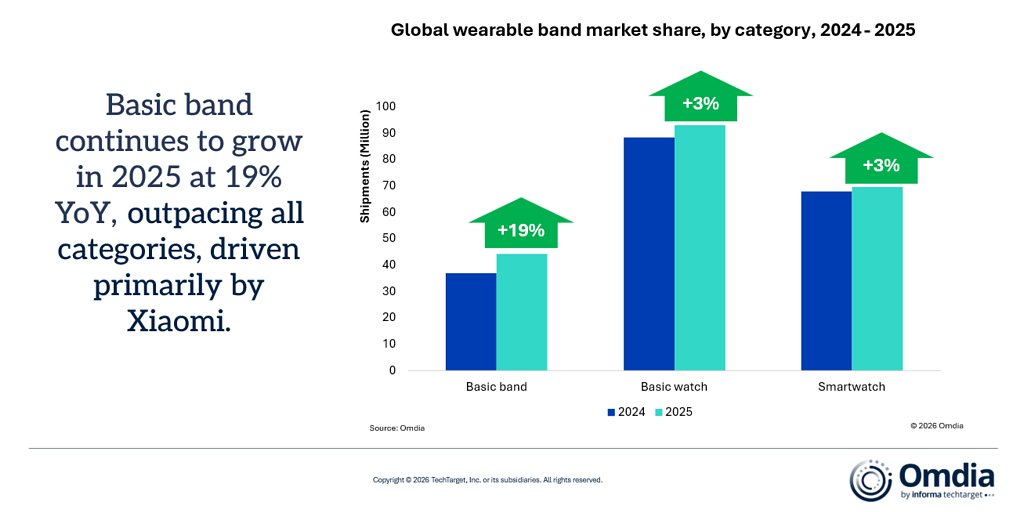

- Global wearable market growth: 6% in 2025, surpassing 200 million units shipped

- Xiaomi's market share: 18%, narrowly edging out Apple (17%) for the top spot

- Top 5 vendors' combined share: 65% (up from 59% in 2024), squeezing smaller competitors

Experts agree that the wearable market is shifting from hardware-driven competition to ecosystem and AI-powered services, with seamless integration and data insights becoming key differentiators.

Xiaomi's Wearable Crown: How Ecosystems and AI Dethroned Hardware

LONDON, UK – February 27, 2026 – The global wearable technology market has a new leader. For the first time since 2020, Chinese electronics giant Xiaomi has claimed the top spot in annual shipments, narrowly edging out perennial front-runner Apple in a market that is fundamentally reshaping itself around software, services, and artificial intelligence.

According to a new report from technology research firm Omdia, which was recently named "Analyst Firm of the Year" by the IIAR>, the global wearable device market grew a steady 6% in 2025, surpassing 200 million units shipped. In this expanding market, Xiaomi captured an 18% share, driven by a sophisticated strategy that extends far beyond its popular, budget-friendly fitness bands. Apple followed closely in second place with a 17% share, while Huawei secured the third position with 16%, highlighting a fiercely competitive landscape where the top three vendors are separated by razor-thin margins.

This shakeup at the top is more than just a change in rankings; it signifies a pivotal industry-wide transformation. The era of competing solely on hardware specifications and design is drawing to a close, replaced by a more complex, strategic battle for ecosystem dominance.

A New Leader in a Shifting Battlefield

Xiaomi’s ascent is not the result of a single hit product but a calculated, multi-category strategy. While its affordable bands continue to drive high volume in the mass market, the company has successfully moved up the value chain with its basic and advanced smartwatches. This vertical move is supported by key investments in in-house chip development and a deep focus on integrating wearables into its expansive "Human × Car × Home" ecosystem.

This approach allows a user's smartwatch to communicate seamlessly with their smartphone, smart home devices, and even future connected vehicles, creating a sticky, interconnected experience. By offering a wide breadth of products at competitive price points, particularly in emerging and price-sensitive markets, Xiaomi has built a massive user base that serves as the foundation for its ecosystem ambitions.

“Wearables are moving from a hardware-driven race to an ecosystem-led competition,” noted Omdia Research Manager Cynthia Chen in the report. “With less than one percentage point separating the top three vendors, competitive advantage now depends on seamless cross-device integration and the ability to deliver monetizable, value-added data services.”

This new reality is forcing every major player to rethink its approach. Apple, despite being nudged to second place in shipment volume, retains an iron grip on the premium segment. Its strategy hinges on leveraging 5G connectivity and a powerful, health-centric ecosystem to foster deep loyalty among its high-value users. Features like advanced hypertension monitoring, combined with the seamless integration of the Apple Watch with iPhones and other services, create a powerful moat that is difficult for competitors to breach.

The End of Hardware Dominance

The intensifying competition is also accelerating market consolidation. The top five vendors—Xiaomi, Apple, Huawei, Samsung (9%), and Garmin (5%)—now command a larger portion of the market than ever before. The share of the "Others" category, comprising smaller brands and niche players, fell from 41% in 2024 to just 35% in 2025. This squeeze suggests that scale, brand recognition, and a comprehensive ecosystem are becoming prerequisites for survival.

Huawei has solidified its position by focusing its efforts on two key growth areas: professional-grade sports tracking and medical-grade health applications. By building out a robust, closed-loop health ecosystem, the company aims to retain users by offering value that transcends the physical device itself. Similarly, Garmin continues to defend its market share by catering to serious athletes and outdoor enthusiasts who demand specialized features and rugged reliability.

The success of smaller, service-first companies like Oura and Whoop, which operate on a subscription-based model with lighter hardware, has provided a blueprint that larger companies are now emulating. The core lesson is that the device is merely the gateway; the ongoing services and data insights are what keep users engaged and paying.

Subscriptions and AI: The New Profit Engines

This shift is leading to a profound structural change in how wearable companies generate revenue. As hardware margins are squeezed by rising component costs and intense price competition, AI-powered features and subscription services are transforming from optional extras into essential drivers of profitability.

“The wearables profit model is undergoing structural change,” stated Omdia Research Director Jason Low. “Algorithms and services are becoming standalone profit centers, with advanced health insights, professional training plans, and AI-powered coaching generating recurring subscription revenue.”

This recurring revenue model provides a critical buffer against the volatility of the hardware market. For consumers, this translates into access to more sophisticated and personalized insights. Wearable devices are increasingly optimized for continuous health monitoring, with some vendors even exploring screenless designs to maximize comfort and ensure uninterrupted data collection. This data, in turn, fuels the AI algorithms that power personalized health reports, fitness plans, and early-warning alerts, creating a virtuous cycle of engagement and value. By increasing usage and stickiness, these services provide more data points that allow for even more tailored and valuable offerings over time.

The Next Frontier: AI and Medical-Grade Health

Looking ahead to 2026 and beyond, the industry's growth trajectory will be defined by advancements in on-device AI and the pursuit of medical-grade health monitoring. Omdia projects modest single-digit growth for the market, but the true battle will be fought over substantive technological breakthroughs. Meaningful upgrade cycles for existing users will no longer be driven by slightly faster processors or new watch face colors, but by the introduction of truly revolutionary health capabilities.

For leading vendors like Apple, Samsung, and Huawei, the holy grail is the integration of reliable, non-invasive monitoring for key physiological metrics—most notably, blood glucose and continuous blood pressure. The first company to successfully crack this complex technological challenge and secure regulatory approval will likely trigger a massive wave of upgrades and capture significant market share.

Smartwatches are expected to be the primary platform for this evolution, combining advanced sensors, powerful on-device AI analytics, and deep ecosystem connectivity. They are rapidly becoming the most scalable platform for integrating personal AI agents, capable of not only tracking health data but also providing proactive coaching and managing other aspects of a user's digital life. As this technological arms race continues, competitive advantage will depend less on shipment volume alone and more on the depth of a company's AI capabilities and the strength of its integrated, cross-device ecosystem.