- 32,000 securities covered by Woodseer Dividend Forecast data

- Over 1,000 academic papers citing OptionMetrics data

- 1996 as the year OptionMetrics began serving institutional clients

Experts view these upgrades as a strategic reinforcement of OptionMetrics' leadership in providing high-quality, research-grade historical options data, essential for modern quantitative finance and empirical analysis.

OptionMetrics Refines 'Gold Standard' Data for Quant Strategists

NEW YORK, NY – February 19, 2026 – OptionMetrics, a prominent provider of historical options data for institutional investors and academic researchers, has announced significant upgrades to its flagship databases, IvyDB US 7.0 and IvyDB ETF 5.0. The enhancements introduce a new level of flexibility and precision, incorporating borrow rate calculations and advanced dividend forecasting to meet the evolving demands of modern quantitative finance.

For over two decades, OptionMetrics' IvyDB has been widely regarded by many in academia and finance as a benchmark for historical options data. This latest release aims to solidify that position by providing more granular tools for asset valuation and strategy development, directly addressing the complex needs of hedge funds, institutional investors, and quantitative analysts who rely on intricate models to navigate the markets.

A New Level of Precision: Inside the Upgrades

The most significant technical advancements in IvyDB US 7.0 and IvyDB ETF 5.0 lie in the new methodologies offered for options data calculations. For the first time, users can choose to incorporate borrow rates—the interest cost of borrowing a stock for a short sale—into their models. This is a critical development, as it allows for a more accurate calculation of a stock's cost-of-carry, a fundamental component of option pricing.

For quantitative analysts, the inclusion of borrow rates is a significant leap from the simplified assumptions often used in traditional pricing models like the Black-Scholes-Merton formula. The cost of borrowing can vary dramatically, especially for “hard-to-borrow” stocks, and this variance directly impacts option premiums. By providing this data, OptionMetrics enables traders to more accurately price options, detect potential arbitrage opportunities by validating put-call parity under real-world borrowing costs, and enhance risk management for strategies involving short positions.

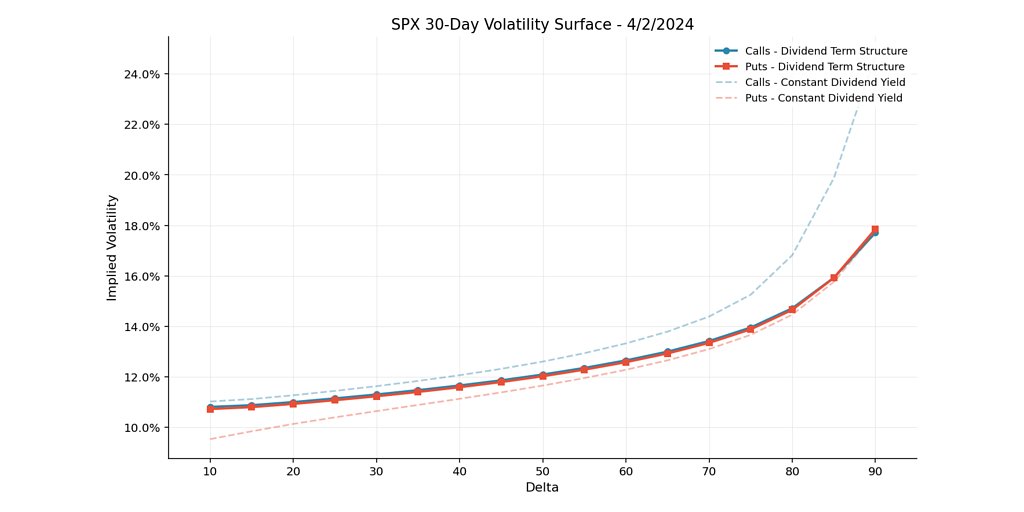

Complementing this is the introduction of implied index yields presented in a term structure format. Instead of relying on a single, static dividend yield for an entire index, users can now access a series of implied yields across different time horizons. This dynamic view reflects the market's evolving expectations for dividend payouts at various maturities, which is crucial for accurately pricing long-dated index options and developing sophisticated dividend-based trading strategies. The granular, time-sensitive data allows for more nuanced modeling of dividend expectations, a vital input for a wide range of quantitative finance applications.

Enhancing Accuracy with Advanced Dividend Forecasting

Another cornerstone of the upgrade is the automatic integration of Woodseer Dividend Forecast data. OptionMetrics acquired Woodseer Global, a specialist in dividend forecasting, and is now embedding its data directly alongside respective securities within the IvyDB datasets. Woodseer has built a strong reputation for its hybrid “algorithm+analyst” methodology, which combines automated data processing with human oversight to deliver highly accurate dividend predictions for over 32,000 securities globally.

This integration serves a dual purpose. First, it provides quantitative finance professionals with a premium, forward-looking dataset to assess and backtest dividend-focused strategies, from income planning to dividend capture. Second, OptionMetrics now uses this leading-edge forecast data as an input for its own calculations, resulting in more accurate security pricing and implied volatility (IV) metrics across the entire database. This creates a virtuous cycle of data refinement, where the inclusion of superior forecast data elevates the quality of the core analytics provided to all users.

“OptionMetrics' IvyDB US 7.0 is our most comprehensive and flexible dataset yet,” said Eran Steinberg, COO at OptionMetrics, in the company’s announcement. “By leveraging borrow rates and including Woodseer Dividend Forecast data alongside the longstanding gold standard in options data, this update provides more precise valuations and richer data for use in options and equities strategies.”

Solidifying a Benchmark in a Competitive Market

These upgrades are widely seen as a strategic move by OptionMetrics to reinforce its position in a competitive financial data market. The company’s claim to providing the “gold standard” in historical options data is supported by its extensive adoption within academia—its data is a staple on the Wharton Research Data Services (WRDS) platform and has been cited in over a thousand academic papers—and its long history serving institutional clients since 1996.

While large financial data platforms like Bloomberg and Refinitiv offer broad market data, and specialized vendors such as IVolatility and Cboe provide their own datasets, OptionMetrics has long differentiated itself with its focus on clean, research-grade historical data specifically curated for empirical analysis. The new features in IvyDB 7.0 are designed to deepen this specialization, offering a level of analytical depth that is difficult for more generalized providers to match.

The enhancements also improve data accessibility, with an improved Genie loader facilitating easier loading via FTP or the cloud data platform Snowflake, ensuring that clients can seamlessly integrate the vast datasets into their proprietary workflows.

Meeting the Demands of Modern Quantitative Finance

The release of IvyDB US 7.0 and IvyDB ETF 5.0 arrives as the quantitative finance industry grapples with an insatiable demand for more granular, accurate, and comprehensive data. The rise of algorithmic trading and the increasing use of artificial intelligence and machine learning have made high-quality historical data a critical resource. These advanced models require vast, clean, and meticulously structured datasets to train algorithms for pattern recognition, predictive analytics, and automated risk management.

By providing more realistic inputs like borrow rates and term-structured dividend yields, OptionMetrics is equipping financial professionals with the tools to build more robust and reliable models. The greater precision in implied volatility and other risk metrics helps traders and portfolio managers better assess risk, identify mispricings, and ultimately contributes to more efficient markets.

The trend toward data-driven decision-making means that access to superior analytics is no longer just an advantage but a necessity for maintaining a competitive edge. The detailed data points included in the latest IvyDB updates allow for a deeper understanding of market dynamics, enabling investors to move beyond simplistic models and capture alpha in an increasingly complex financial landscape.