- $2.24 billion: Excess federal taxes levied on cannabis operators in 2025 due to IRS Code Section 280E

- 70%: Effective federal tax rate faced by cannabis firms, far exceeding the standard 21% corporate rate

- $27 billion: Total federal taxes paid by the cannabis industry since 2018, with $15 billion attributed to Section 280E

Experts argue that the archaic federal tax provision Section 280E is crippling the legal cannabis industry, creating an unsustainable financial burden that stifles growth and forces businesses to operate at a severe disadvantage compared to other legal industries.

Cannabis Firms Face Crippling 70% Tax Rates Under Archaic Federal Law

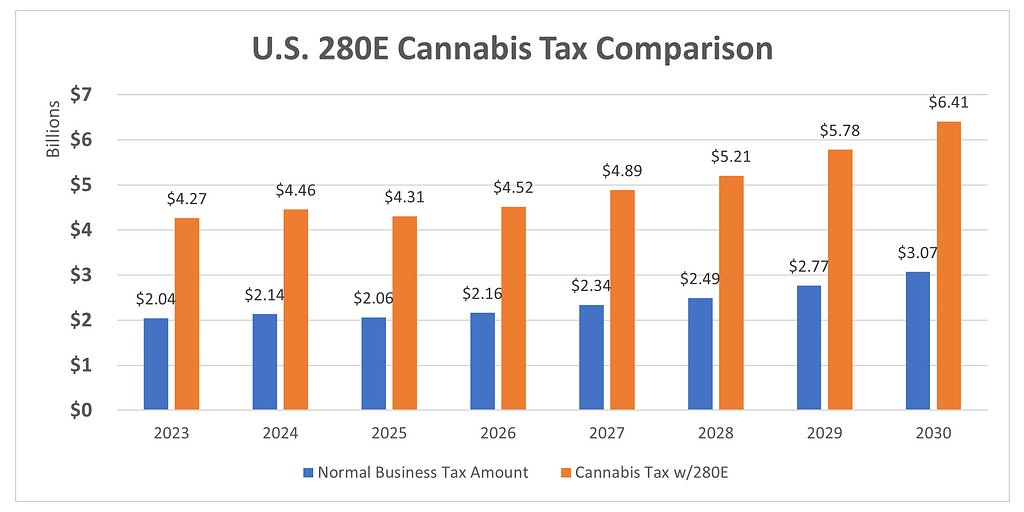

PORTLAND, OR – April 09, 2026 – America’s state-legal cannabis industry is being taxed into oblivion by an obscure, 40-year-old federal tax provision, according to a refreshed analysis by Whitney Economics. The report reveals a staggering financial burden, with an estimated $2.24 billion in excess federal taxes levied on cannabis operators in 2025 alone due to the punitive nature of IRS Code Section 280E.

This immense tax liability stems from a fundamental conflict: while 38 states have legalized cannabis for medical or adult use, the plant remains a federally prohibited Schedule I substance under the Controlled Substances Act (CSA). This classification triggers Section 280E, a rule originally designed to punish illicit drug traffickers, which now places a chokehold on legitimate, state-licensed businesses.

“The amount of additional taxes cannabis operators pay is staggering,” said Beau Whitney, Chief Economist at Whitney Economics, a leading cannabis research firm. “The industry is being taxed out of business.” Since 2018, the firm estimates that the cannabis industry has paid over $27 billion in federal taxes, with a colossal $15 billion of that being excess taxes directly attributable to 280E.

The Punitive Legacy of a Decades-Old Law

Enacted in 1982 during the height of the “War on Drugs,” Section 280E was Congress’s response to a court case where a convicted drug dealer was permitted to deduct business expenses like rent and car payments. The law explicitly forbids any business “trafficking” in Schedule I or II controlled substances from deducting ordinary and necessary business expenses from their gross income.

For a typical American business, deductions for rent, employee payroll, marketing, legal fees, utilities, and security are standard practice, lowering their taxable income. For a cannabis dispensary or cultivator, these deductions are disallowed. The only significant exception is the Cost of Goods Sold (COGS), which primarily includes the direct costs of producing or acquiring the product. This distinction disproportionately harms retailers, whose major expenses—like rent for their storefronts and wages for their budtenders—do not qualify as COGS.

The result is an effective federal tax rate that can soar to 70% or higher, a figure unheard of in any other legal industry, where the standard corporate tax rate is 21%. This forces companies to pay taxes on their gross profits, not their net income, creating severe cash flow crises even for businesses that are otherwise profitable on paper. It’s a policy that industry insiders argue treats state-licensed entrepreneurs like criminals under federal tax law.

A Policy Paradox Stifling Growth

The application of 280E creates a deep policy paradox that undermines the economic potential of state-legal markets. While states embrace cannabis for its tax revenue and job creation, the federal government’s tax policy actively works to destabilize those same businesses. This financial strain makes it nearly impossible for operators to reinvest in their companies, expand operations, hire more staff, or offer competitive wages and benefits.

Furthermore, the heavy tax burden makes it difficult for legal operators to compete with the illicit market, which operates without any tax obligations or regulatory costs. As legal businesses are forced to keep prices higher to cover their exorbitant tax bills, consumers may be driven back to the unregulated, and often unsafe, black market.

This pressure is now creating a domino effect at the state level. “With pricing compression occurring in every major U.S. cannabis market, tax revenues will no longer be the goose that laid the golden egg,” Whitney warned. “In fact, declining state cannabis tax revenues are resulting in state cannabis tax increases, which will further hurt revenues, making the overall tax situation untenable for the industry.”

Rescheduling: A Beacon of Hope on the Horizon

Relief may be on the way, however, in the form of federal rescheduling. In a landmark move, the Department of Health and Human Services (HHS) officially recommended in August 2023 that the Drug Enforcement Administration (DEA) reclassify cannabis from Schedule I to Schedule III of the CSA. The DEA is currently conducting its final review.

This move would be a seismic shift for the industry. Because Section 280E only applies to substances in Schedules I and II, rescheduling to Schedule III would immediately render it inapplicable to cannabis businesses. Operators would finally be able to deduct all ordinary business expenses, aligning their tax obligations with every other legal industry in the country.

The economic impact would be profound. Freeing up billions of dollars in cash flow would ignite a wave of investment, expansion, and job creation. It would improve business valuations, attract new institutional capital that has remained on the sidelines, and allow companies to innovate and lower prices for consumers.

“This would be a major boost to an industry struggling with cash flow and profitability,” the Whitney Economics report notes, adding that it would also “increase business valuations and would attract new investment.”

A Call for Discipline Amid Uncertainty

Despite the widespread optimism, the timeline for a final decision from the DEA remains speculative, leaving operators in a precarious position. Federal agencies move at their own pace, and political dynamics, including what Whitney called “the change of the U.S. Attorney General,” add another layer of uncertainty.

Until reform is official, 280E remains the law of the land. Industry leaders are cautioning businesses against banking their survival on a policy change that has not yet materialized. The advice from experts is clear: maintain strict fiscal discipline and build a business model that can withstand the current harsh tax environment.

“We are advising operators in the industry to remain fiscally disciplined, despite the prospect of future reform,” Whitney stated. “Too many operators may be counting on this reform for their survival. They need to stay the course but be prepared to pivot quickly once the tax policy change occurs.”

For thousands of cannabis entrepreneurs, the wait is an exercise in endurance. They continue to navigate a system that simultaneously licenses them as legitimate businesses and penalizes them as illegal traffickers, all while hoping that federal policy will soon catch up to the reality of the thriving legal marketplace they have built.