America's Warehouse Divide: Big Boxes Boom, Small Spaces Struggle

- Big-box warehouse demand surge: 80.7% year-over-year increase in leasing for spaces ≥500,000 sq. ft. (Q1 2026).

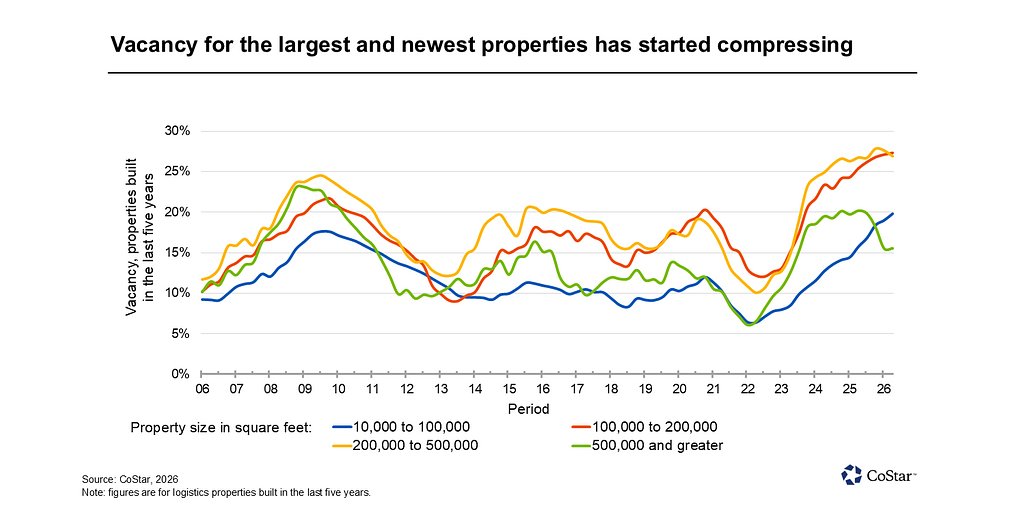

- Mid-sized warehouse struggle: Vacancy rates at highest levels since 2006 for 200,000–500,000 sq. ft. properties.

- Lease term compression: Average lease duration for large properties dropped from 7 to 5 years (2022–2026).

Experts agree the industrial real estate market is undergoing a structural realignment, with big-box warehouses thriving while mid-sized and small properties face oversupply challenges and slower absorption.

America's Warehouse Divide: Big Boxes Boom, Small Spaces Struggle

ARLINGTON, VA – June 16, 2026 – The vast, uniform landscape of American industrial real estate is developing deep fractures. From the outside, the endless rows of concrete tilt-up buildings look the same, but inside, a tale of two markets is unfolding. On one side, mega-warehouses—sprawling facilities larger than ten football fields—are in high demand, with vacancy rates shrinking. On the other, their smaller and mid-sized cousins are feeling the pressure of new supply and slower absorption, a dynamic that complicates the simple narrative of a post-pandemic logistics boom.

Recent data from CoStar Group reveals this stark bifurcation. Demand for newer industrial properties exceeding 500,000 square feet has rebounded strongly since the latter half of 2025, pulling vacancy rates for the largest assets down. Yet, for newly built properties between 200,000 and 500,000 square feet, the story is different. Vacancy rates are at their highest levels since 2006, signaling a market struggling to digest a recent surge in construction.

This isn't a simple boom or bust; it's a fundamental realignment. The systems that move goods across the country are being reshaped by economic uncertainty, and the buildings that house those systems are reflecting the strain.

A Tale of Two Warehouses

Beneath a national industrial vacancy rate that has stabilized between 6.7% and 7.6%, depending on the analyst, lies a deep divergence. The market for big-box facilities is thriving. One leading real estate services firm reported a staggering 80.7% year-over-year surge in leasing for spaces of 500,000 square feet or more in the first quarter of 2026. Another noted that over 50 such leases were signed in the same period, a first for the industry. Large logistics occupiers, after a period of caution, are returning to the market, driving absorption and signaling renewed confidence.

Meanwhile, the middle of the market is getting squeezed. A glut of new, mid-sized warehouses is taking longer to fill. This oversupply is a direct result of a speculative building boom that met the headwinds of economic uncertainty. As one analyst noted, the market has moved past peak uncertainty, but the hangover from the development frenzy remains.

Even the small-bay segment—properties typically under 50,000 square feet that cater to local businesses—presents a complex picture. While its overall vacancy rate of 6.4% is significantly tighter than the broader market, elevated economic uncertainty has weighed on small-business expansion plans. This has led to slower absorption for newly delivered space, even as the segment as a whole suffers from a structural lack of new supply over the past decade.

The New Premium on Flexibility

Perhaps the most telling indicator of the new market reality is not just what space is being leased, but how. According to CoStar, the average lease term for the largest industrial properties has compressed significantly, falling from around seven years in 2022 to just five years today. This shift reveals a deep-seated anxiety among tenants.

“These shifts reflect a combination of supply chain volatility, evolving trade dynamics, and changing consumer demand, all of which have increased the perceived risk of long-term commitments,” explained Juan Arias, national director of industrial analytics at CoStar Group. “In response, tenants are favoring shorter lease terms that offer greater flexibility to adjust their footprints as business conditions evolve.”

This desire for agility is rewriting commercial contracts. The static, long-term footprint is being replaced by what industry experts call an "elastic portfolio." Businesses are hedging against geopolitical tensions, trade policy volatility, and the unpredictable whims of consumer demand. A ten-year lease on a massive distribution center becomes a significant liability if trade routes shift or a key product line is discontinued. The result is a preference for shorter commitments, more flexible terms, and even co-warehousing models that allow businesses to scale space up or down on a near-monthly basis. This trend presents a challenge for landlords and investors who have long relied on the stability of long-term leases for their financial models.

A National Trend with Local Realities

The story of this divided market becomes even more complex at the local level. What is true for the nation is not necessarily true for Phoenix or Omaha. Regional dynamics, driven by land availability, local economic health, and development pipelines, are creating a patchwork of hotspots and headaches.

Phoenix, for instance, continues to report one of the highest vacancy rates among major markets, standing at 10.6% in the first quarter. This is despite leading the nation in absorption gains, a sign of how much new supply the market is still working to digest. Austin is facing similar pressures. These sunbelt darlings, once magnets for growth, are now contending with the consequences of their own rapid expansion.

In stark contrast, markets with natural or legislative constraints on land supply exhibit extreme tightness. Vacancy in Omaha sits at a mere 2.4%, while Miami and Orange County hover around 4%. In these areas, businesses face intense competition for any available space. The story is different again in places like California's Inland Empire, a logistics behemoth, where vacancy is now approaching 10% and rents have fallen over 17% from their peak, signaling a clear oversupply.

These regional disparities underscore a fundamental truth: industrial real estate is not a monolith. The national average is just that—an average that obscures the unique challenges and opportunities playing out in cities and corridors across the country.

The Developer's Dilemma

In response to this fractured landscape, developers and investors are becoming more cautious and strategic. The era of speculative development—building warehouses without a tenant already signed—is tapering off. New construction starts are slowing, and completions were down 27% year-over-year in the first quarter of 2026. The development pipeline is not only shrinking but also changing in character.

Build-to-suit projects, custom-built for a specific tenant, now account for a significant portion—as much as 40%—of the space under construction. This reflects both developer caution and occupier demand for specialized, high-performance facilities ready for advanced automation. A clear "flight to quality" is underway, with investors and tenants alike prioritizing modern buildings with higher power capacity and clear heights, leaving older, less functional assets behind.

The market bifurcation is forcing a strategic pivot. For investors, the focus is shifting from chasing explosive rent growth to securing stable income from high-quality assets. For developers, it means a more disciplined approach, often involving retrofitting existing properties or focusing on the structurally undersupplied small-bay segment. The game is no longer just about building bigger, but about building smarter for a market where flexibility has become the most valuable commodity of all.

📝 This article is still being updated

Are you a relevant expert who could contribute your opinion or insights to this article? We'd love to hear from you. We will give you full credit for your contribution.

Contribute Your Expertise →