- Used Jet Prices: Down 4.9% year-over-year (YOY) in March 2026, with large jets falling 7.6% YOY.

- Helicopter Inventory: Robinson Piston Helicopters saw a 40% YOY surge in inventory, while asking prices rose 4.29% YOY.

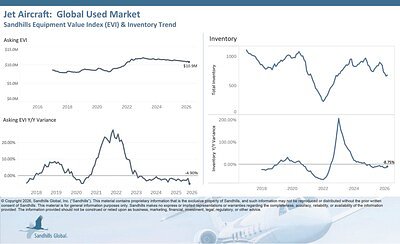

- Jet Inventory: Overall pre-owned jet inventory down 8.75% YOY, with piston-single aircraft inventory plummeting 15.2% YOY.

Experts conclude that the pre-owned aircraft market is undergoing a rebalancing, with cooling trends in jets and turboprops contrasting sharply with a booming helicopter segment driven by strong demand and supply shifts.

Used Jet Prices Descend While Helicopter Market Climbs

LINCOLN, Neb. – April 06, 2026 – The pre-owned aircraft market is presenting a study in contrasts, with new data revealing a significant cooling trend for used jets, turboprops, and piston-single planes, even as the helicopter segment experiences a surprising and dramatic upswing. According to the March 2026 aviation market reports from Sandhills Global, the high-flying prices and scarce inventory that defined the post-pandemic boom are giving way to a more nuanced and segmented marketplace.

For prospective buyers who have been waiting on the sidelines, this shift could signal a long-awaited window of opportunity. However, the data also reveals that market dynamics vary wildly by aircraft category, rewarding those who can navigate the complex crosscurrents.

A Market in Rebalance

After years of a frenetic seller's market, the fixed-wing aircraft sector is showing clear signs of stabilization. The latest Sandhills report indicates that asking prices for used jets have continued an 11-month-long downward trend, dipping 4.9% year-over-year (YOY) in March. The decline was even more pronounced in the used large jet category, which saw asking prices fall 7.6% YOY.

Inventory levels, while fluctuating month-to-month, are also lower than the previous year across most key segments. The overall pre-owned jet inventory was down 8.75% YOY. Similarly, the U.S. and Canada market for used piston-single aircraft saw inventory plummet by 15.2% YOY, with asking prices also easing slightly. Used turboprop aircraft followed a similar pattern, with both inventory and asking prices falling compared to the year prior.

While these figures point to a cooling market, other industry analyses provide crucial context. Reports from early 2026 indicated that the percentage of the global business jet fleet available for sale remained historically low, hovering around 4%, which is significantly below the 8-10% range typically associated with a balanced market. This suggests that while the pricing fever has broken, the market is not facing a collapse. Instead, it is undergoing a rebalancing. Sellers of high-quality, low-time, and program-enrolled aircraft continue to hold a strong position, but buyers now have more negotiating power than they have had in years.

The Helicopter Enigma

While the market for jets and planes cools, the data reveals a completely different story in the rotorcraft world. The market for used Robinson Piston Helicopters, a bellwether for the segment, is experiencing a remarkable boom. Sandhills' March data shows a staggering 40% YOY surge in inventory for these helicopters.

This represents a dramatic and rapid reversal from just two months prior. In January 2026, the same data set showed Robinson helicopter inventory was down 7.69% YOY. The sudden flood of available units onto the market is a significant development. Even more curiously, this massive increase in supply has not dampened prices. Asking prices for used Robinson helicopters climbed 4.29% YOY, indicating that powerful demand is absorbing the new inventory.

Robinson Helicopter Company overwhelmingly dominates the global piston market, accounting for 85-90% of certified production. These helicopters are workhorses, widely used for initial pilot training, personal flight, and various commercial operations. The surge could be driven by multiple factors, including flight schools expanding their fleets, a new wave of private pilots entering the market, or operators upgrading to newer models. The strong underlying demand for helicopters across diverse sectors—from emergency services to energy and tourism—coupled with long OEM backlogs, continues to fuel a robust pre-owned market.

Economic Forces and Market Drivers

The shifting aviation landscape is being shaped by powerful macroeconomic forces. A significant tailwind, particularly in the United States, has been the reinstatement of 100% bonus depreciation for 2025. This tax incentive has accelerated purchasing decisions, pulling demand forward into early 2026 and creating a strong appetite for acquisitions across all jet categories.

Furthermore, improved financing conditions and competitive terms from specialist lenders have made aircraft acquisitions more accessible for well-qualified buyers. While the global economic outlook projects a slight deceleration, the U.S. economy remains a pillar of strength, sustaining demand. However, the most significant factor propping up the pre-owned market is the persistent backlog at original equipment manufacturers (OEMs). With delivery slots for new jets and helicopters stretching two years or more, buyers with immediate needs are compelled to turn to the pre-owned market. This dynamic ensures that demand for desirable, late-model aircraft remains firm, creating a floor under prices even as the broader market softens.

Charting the Skies with Data

Navigating this multifaceted and diverging market requires more than just a general sense of the trends; it demands precise, granular data. This is where market intelligence from firms like Sandhills Global becomes indispensable. The company’s detailed reports, powered by its proprietary Sandhills Equipment Value Index (EVI), allow stakeholders to look beyond headline numbers and understand the nuances of specific asset classes.

For example, the March report highlights that while the overall jet market is cooling, the used mid-jet category saw inventory jump over 10% month-over-month, whereas the used super mid-jet segment experienced a 12% YOY inventory decline. This level of detail is critical for an operator deciding whether to buy, sell, or hold a multi-million-dollar asset. Recognizing the need for precision, Sandhills recently enhanced its EVI methodology, recalculating historical metrics to improve accuracy and provide a clearer picture of market movements.

This commitment to refining data analytics underscores a fundamental shift in the industry. In a market no longer defined by a single, universal upward trajectory, success hinges on understanding the specific dynamics of each segment. As the trends for jets, turboprops, and helicopters continue to follow their own unique paths, access to accurate and timely data is no longer just an advantage—it is an essential tool for navigating the shifting skies of the pre-owned aviation marketplace.

Topics & Related

Regulatory & Legal

Sustainability & Climate

Geopolitics & Trade

Manufacturing & Industrial

Related Company Pulse