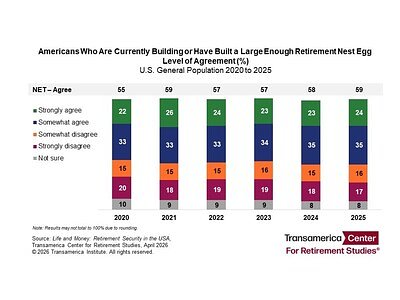

- 59% of Americans feel they are building a large enough retirement nest egg, up only slightly from 55% in 2020.

- 66% of Americans confident in retiring comfortably, a figure unchanged for five years.

- 38% of Americans fear Social Security will be reduced or cease to exist, with projections showing potential insolvency by 2032.

Experts agree that systemic economic pressures, financial literacy gaps, and policy challenges are undermining retirement security for many Americans, requiring both individual action and broader policy reforms to address the issue.

US Retirement Dream Stalls Amid Economic and Future Fears

LOS ANGELES, CA – April 16, 2026 – The promise of a secure retirement, a cornerstone of the American dream, is stuck in the doldrums for millions. A major new report reveals that despite the years passed since the global pandemic, Americans' confidence in their financial future has shown little to no improvement, battered by persistent economic headwinds, deep-seated anxieties about the future, and a growing sense of personal financial strain.

According to the “Life and Money: Retirement Security in the USA” report released today by the nonprofit Transamerica Center for Retirement Studies® (TCRS), fewer than six in 10 Americans (59%) feel they are building a large enough retirement nest egg. This marks only a marginal improvement from 55% in 2020. More strikingly, the percentage of Americans confident in their ability to retire comfortably has remained completely flat at 66% over the last five years.

“Retirement is a core tenet of the American dream. It is a chapter in life that brings time and freedom for travel, family and friends, hobbies, and giving back to our communities,” said Catherine Collinson, CEO and president of Transamerica Institute and TCRS. “Today, a secure retirement may be out of reach for many Americans.”

While median household retirement savings have increased from $44,000 to $56,000 since 2020, the data suggests this growth has not been enough to move the needle on overall confidence, pointing to deeper, more systemic challenges facing households across the country.

Economic Headwinds and Looming Anxieties

The stagnation in retirement outlook is not happening in a vacuum. The report highlights a confluence of pressures that are actively undermining Americans' ability to save and plan for the long term. As Collinson noted, “Americans are navigating a turbulent economy, the high cost of living, the impacts of AI and robotics on the future of work, and the nerve-wracking countdown to the depletion of the Social Security trust funds.”

These are not abstract concerns. Persistent inflation continues to erode purchasing power and strain household budgets. In 2025, the Consumer Price Index saw notable increases in the costs of food (3.1%), energy (2.3%), and medical care (3.2%), making it harder for many to cover daily expenses, let alone set money aside for the future. The survey found that 56% of Americans say the economy has negatively impacted their day-to-day life, and 34% list “just getting by to cover basic living expenses” as a top financial priority, competing directly with retirement savings.

One of the most significant fears haunting Americans is the future of Social Security. The report found that 38% of people fear it will be reduced or cease to exist. This anxiety is validated by stark government projections. The Congressional Budget Office (CBO) recently forecast that the program's primary trust fund could be insolvent by 2032, potentially triggering an automatic 28% cut in benefits for 72 million recipients if Congress fails to act.

Adding another layer of uncertainty is the rapid advancement of artificial intelligence. Nearly half of non-retired workers (46%) now worry that AI and robotics will make their job skills obsolete. This concern reflects expert analysis, with a 2025 McKinsey Global Institute report suggesting that around 40% of U.S. jobs are “highly automatable,” particularly those involving routine data processing and administrative functions. These combined pressures contribute to a pervasive sense of fatigue, with 46% of Americans reporting they often feel exhausted and burnt out.

A Paradox in Personal Finance

While external forces pose significant challenges, the report also points to a critical gap in individual financial preparedness. A staggering 62% of Americans agree they could work their entire lives and still not save enough for retirement. This sentiment exists alongside a clear deficit in financial literacy and planning: only 20% of Americans claim to have “a lot” of knowledge about personal finance, and fewer than one in four (23%) have a formal, written retirement strategy.

This creates a paradox. Other industry data shows that retirement account balances have been growing. Vanguard’s 2025 “How America Saves” report, for instance, found that average participant account balances hit a record high of $167,960. Similarly, Fidelity reported that the average 401(k) balance for long-term savers on its platform rose to $304,200.

However, these rising balances mask the underlying fragility. The same reports that show record balances also reveal high rates of hardship withdrawals, as families tap into their future to cover present emergencies. With competing priorities like building emergency savings (38%) and paying off high-interest credit card debt (33%), many find themselves in a constant financial triage, unable to fully focus on long-term goals. Experts stress the importance of fundamental financial practices, such as creating a budget, paying down debt, and leveraging tools like automated contributions to maximize savings. The SECURE 2.0 Act has increased contribution limits for 2026 to $24,500 for 401(k)s and $7,500 for IRAs, offering a path for those who can afford it to accelerate their savings.

A Call for Systemic Support and Policy Action

While individual action is crucial, there is a growing consensus that personal responsibility alone cannot solve a systemic problem. The report underscores the need for broader policy interventions to strengthen the nation's retirement infrastructure.

“Strengthening the U.S. retirement system requires addressing the ever-changing realities Americans are facing,” Collinson stated, calling for public-private partnerships to “ensure the sustainability of safety nets, such as Social Security and Medicare, and future-proof our retirement system.”

Policymakers have begun to take steps. The ongoing implementation of the SECURE 2.0 Act is a significant move, with provisions rolling out in 2025 that mandate automatic enrollment in new 401(k) plans and increase catch-up contribution limits for workers aged 60 to 63. A national database to help workers find lost retirement accounts is also in development.

Furthermore, new bipartisan legislation is being considered to address specific gaps. The “Improving Retirement Security for Family Caregivers Act,” reintroduced in April 2026, aims to help caregivers who leave the workforce save for retirement by expanding IRA access. Another proposal, the “Helping Young Americans Save for Retirement Act,” seeks to lower the minimum participation age for company retirement plans from 21 to 18, allowing younger workers to start saving earlier.

These legislative efforts, combined with industry initiatives, represent a multi-pronged approach to a complex challenge. Securing the American retirement dream for current and future generations will require a sustained commitment from individuals to plan and save, and a parallel commitment from policymakers to fortify the systems that make those savings possible and secure.