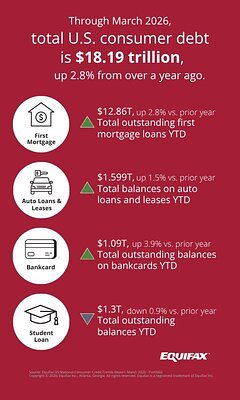

- Total U.S. consumer debt: $18.19 trillion (up 2.8% from the previous year)

- Subprime bankcard accounts: Increased by 18.6% year-over-year

- Student loan delinquency rate: 17.01% (90+ days past due, fourth consecutive monthly increase)

Experts warn of a deepening 'K-shaped' economic divide, with subprime borrowers increasingly relying on credit to manage essential expenses while student loan delinquencies signal broader financial instability.

US Consumer Debt Hits Record $18.2T Amid Deepening Economic Divide

ATLANTA, GA – May 28, 2026 – Total U.S. consumer debt has surged to an unprecedented $18.19 trillion, according to a new first-quarter report from Equifax. The record-breaking figure, up 2.8% from the previous year, reveals a starkly divided American economic landscape where financial stability is diverging, creating a deepening 'K-shaped' reality for millions.

While some indicators suggest resilience, the data paints a complex and troubling picture. The growth in debt is largely fueled by a dramatic increase in subprime borrowers turning to credit cards to manage daily expenses. Simultaneously, a fourth consecutive month of rising student loan delinquencies signals a potential crisis that could ripple through the broader economy, challenging the traditional hierarchy of consumer payment priorities.

A Tale of Two Consumers: The Widening Credit Divide

The story of America's record debt is a tale of two very different consumer experiences. On one hand, the population of super-prime borrowers with excellent credit has reportedly grown, indicating a segment of the population is building financial strength. On the other hand, a significant and growing number of consumers with lower credit scores are becoming increasingly dependent on revolving credit to make ends meet.

Equifax's report highlights a dramatic surge in this subprime market. The number of new bankcard accounts opened by subprime borrowers skyrocketed by 18.6% year-over-year as of January 2026. Lenders also expanded access to this group, increasing their total credit limits by a staggering 37.6% compared to the previous year. This expansion in bankcard balances, which grew nearly 4% year-over-year, is outpacing the March 2026 inflation rate of 3.3%, underscoring a reliance on credit that goes beyond discretionary spending.

This trend suggests a fundamental shift in the role of credit for financially vulnerable households. "We are seeing an expansion in the subprime market that underscores the widening gap of the K-shaped economy," said Maria Urtubey, an Equifax Advisor. "Lenders originating more bankcard accounts for consumers in subprime while also increasing total credit limits suggests that, for the lower economic tier, credit may have moved beyond a financial tool and may be becoming a necessity for managing the rising costs of living."

This necessity is driven by persistent economic pressures. With inflation recently ticking up to 3.8% and outpacing nominal wage growth of 3.6%, many households are finding their paychecks stretched thin. The average monthly cost for a financed new vehicle has climbed to a record $773, while housing and other essentials continue to consume a large portion of household budgets, pushing more individuals toward high-interest credit.

The Gathering Storm of Student Debt

While the subprime credit card market expands, a different storm is gathering in the student loan sector. The report reveals a severe and worsening delinquency crisis. The rate of student loans 90 or more days past due reached 17.01% in March, marking the fourth straight monthly increase. This trend, also confirmed by analysis from the Federal Reserve Bank of New York, follows the end of the pandemic-era payment forbearance, which had paused defaults for millions of borrowers.

Even as the number of new student loans being originated has declined, the total dollar amount of these new loans has risen by 4.7%, a clear reflection of the relentlessly increasing cost of higher education. This means new borrowers are starting their financial lives with a heavier burden, while existing borrowers struggle to re-enter a payment system many have not navigated for years.

The consequences of this trend could be far-reaching. Historically, consumers have prioritized making payments on secured debts like mortgages and auto loans over unsecured student loans. However, the sheer scale of the current student debt crisis and the restart of stricter enforcement measures could upend this behavior.

"Historically, consumers have prioritized mortgage and auto payments over student loans," Urtubey noted. "However, as stricter enforcement measures are restarted, we may begin to see disruption in this 'payment hierarchy', potentially introducing stress into other credit categories."

A Complicated Picture of Delinquency and Risk

Beneath the headline numbers for total debt and student loans, the report offers a more nuanced, and at times contradictory, view of consumer financial health. Outside of the student loan portfolio, delinquency rates for most other forms of credit showed signs of improvement. Delinquencies for bankcards, unsecured personal loans, and auto loans all decreased month-over-month and, in some cases, year-over-year.

This positive trend, however, is contrasted by a sharp increase in write-off rates, particularly for bankcards and auto loans. A write-off, or charge-off, occurs when a lender deems a debt unlikely to be collected and removes it from its books as a loss. Typically, delinquencies and write-offs move in tandem. The current divergence suggests two things are happening at once.

First, the rising write-offs are a lagging indicator, representing a final accounting for loans that became delinquent months ago. Second, it signals that lenders are taking a more proactive and strategic approach to risk management. By writing off bad debt now, financial institutions are "rationalizing their balance sheets" for the 2026 fiscal year, effectively cleaning their portfolios to achieve a more sustainable baseline of risk.

This tightrope walk—extending new credit to subprime borrowers while simultaneously clearing out old, non-performing loans—highlights the complex calculations lenders are making in a volatile market. For consumers, the improving delinquency rates may offer a glimmer of resilience. For the financial system, the rising write-offs represent a necessary, if sometimes painful, adjustment to maintain stability in an economy defined by growing inequality and record-breaking debt.