The Middle-Income Squeeze: Why Official Numbers Don't Tell the Full Story

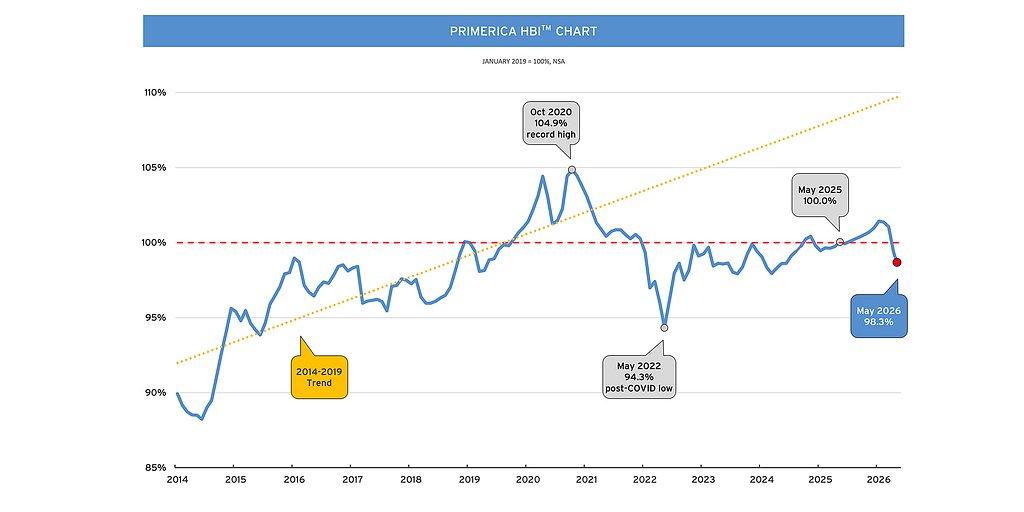

- HBI™ Index: 98.3% in May 2026 (1.7% decline year-over-year)

- Income vs. Costs: Middle-income households saw a 2.5% income increase, but essential costs rose by 6.2%

- Gas Prices: Up 8.6% in May 2026, a major driver of financial strain

Experts agree that middle-income families face a growing financial squeeze due to rising essential costs outpacing wage growth, highlighting the limitations of broad economic indicators like the CPI.

The Middle-Income Squeeze: Why Official Numbers Don't Tell the Full Story

DULUTH, GA – June 30, 2026 – In the often-conflicting narrative of the modern economy, headline figures frequently paint a picture of resilience and recovery. Yet, for a vast swath of the American populace, this optimism feels disconnected from the reality of balancing a household budget. A specialized economic metric released this month throws this disparity into sharp relief, revealing a silent but persistent squeeze on the financial stability of middle-income families.

The latest Primerica Household Budget Index™ (HBI™), a monthly metric tracking the purchasing power of households earning between $30,000 and $130,000, registered at 98.3% for May. This figure, benchmarked against a baseline of 100% in January 2019, signifies a continued erosion of financial standing, marking a 1.1% drop from April and a 1.7% decline from the same time last year. The data reveals a troubling divergence: while earned income for this group saw a modest 2.5% year-over-year increase, the cost of their essential needs soared by 6.2%, creating a deficit that no amount of positive spin can erase.

A Tale of Two Economies

The primary driver of this financial pressure, according to the May HBI™ data, remains the cost at the gas pump. While the rate of increase slowed from its April peak, gas prices were still up 8.6% in May, a significant and unavoidable expense for families commuting to work, school, and stores. This single line item underscores a fundamental challenge: the items whose costs are rising fastest are often the least discretionary.

This is where the HBI™ provides a crucial perspective that broader indicators like the Consumer Price Index (CPI) can miss. While the overall CPI, which measures inflation for a comprehensive basket of goods for all U.S. households, rose a more moderate 4.2% in May from a year ago, the HBI™ focuses specifically on a basket of necessities: food, utilities, gas, auto insurance, and health care. The 6.2% year-over-year surge in this necessity-focused basket highlights that the families who form the backbone of the economy are experiencing a personalized inflation rate far higher than the national average.

"For middle-income families whose paychecks are still being stretched by the cost of everyday necessities, the pressure is very real," noted Glenn Williams, CEO of Primerica, in the release accompanying the data. While he points to encouraging wage growth and potential relief at the pump, the underlying numbers reveal an ongoing struggle. This is the tale of two economies: one reflected in aggregate national statistics, and another lived daily in the households that comprise over half the U.S. population.

This statistical divergence is not just an academic curiosity; it's the source of significant financial and emotional strain. Anecdotal evidence strongly supports the HBI's findings. Families report feeling perpetually behind, even with pay raises. "My salary went up, but so did everything else, and then some," one suburban parent and office manager explained. "The extra money vanishes before it even hits my account, swallowed by gas and groceries. We're not getting ahead; we're just treading water faster."

The Power of a Sharper Lens

The existence of an index like the HBI™ speaks to a growing recognition that one-size-fits-all economic metrics are insufficient for navigating a complex modern economy. By isolating a specific demographic and a specific basket of goods, the index acts as a high-resolution lens, bringing a critical, and often overlooked, segment of the economy into focus. Its methodology is rooted in established, credible sources—including the U.S. Bureau of Labor Statistics and the Federal Reserve Bank of Kansas City—and is overseen by Dr. Amy Crews Cutts, an economist with decades of experience at institutions like Freddie Mac and Equifax.

This rigorous, targeted approach allows for a more nuanced understanding of economic health. It demonstrates that while overall inflation may be moderating, the composition of that inflation matters immensely. A price increase on a luxury good is an inconvenience; a sustained increase in the cost of fuel, food, and utilities is a systemic threat to household stability. For businesses, this insight is invaluable for forecasting consumer demand and resilience. For policymakers, it's a clear signal that broad-stroke solutions may fail to address the acute pressures facing the middle class.

According to economic experts, this targeted analysis is essential for understanding the true impact of our economic environment. "We are in a new paradigm of permanently higher prices that consumers have not yet adjusted to emotionally and, in some cases, financially," one economist familiar with the data noted. The HBI™ quantifies this adjustment gap, showing that even as wages climb, the gains are not enough to offset the higher cost floor for a life of basic necessities.

A Strategic Compass in a Volatile Market

It is no coincidence that this granular analysis comes from Primerica, a financial services company whose entire business model is built around serving middle-income families. The creation and promotion of the HBI™ is a masterstroke of strategic alignment, positioning the firm not just as a service provider, a seller of term life insurance and mutual funds, but as a thought leader deeply invested in the well-being of its core clientele.

By defining and measuring the primary economic challenges facing this demographic, the company gains unparalleled insight that informs its operations from the top down. The HBI™ data provides a real-time feedback loop, helping the firm's vast network of representatives understand the specific pressures their clients are facing. It transforms a sales conversation about financial planning into a deeply relevant discussion about navigating a 6.2% spike in living costs on a 2.5% raise. This builds trust and credibility in a way that generic marketing cannot.

While one must always consider the source, the index's transparent methodology and reliance on public data provide a strong defense against claims of pure self-interest. Rather than obscuring the data, the firm is shining a bright light on a problem that its services are designed to address. It is a sophisticated strategy that marries corporate social responsibility with business intelligence.

With over 5.5 million lives insured and approximately 3.1 million client investment accounts, the company has a significant stake in the financial health of the middle class. The HBI™ is, in essence, a proprietary compass. It helps the organization navigate the volatile economic seas by keeping a firm, data-driven hand on the pulse of the very people it serves. As businesses and governments chart a course through a world in flux, indices like the HBI serve as a critical reminder that the true health of an economy is not just found in the headline numbers, but in the financial reality of the households that power it.

📝 This article is still being updated

Are you a relevant expert who could contribute your opinion or insights to this article? We'd love to hear from you. We will give you full credit for your contribution.

Contribute Your Expertise →