- National Average Premium (2026): $2,158 (up 1% from 2025)

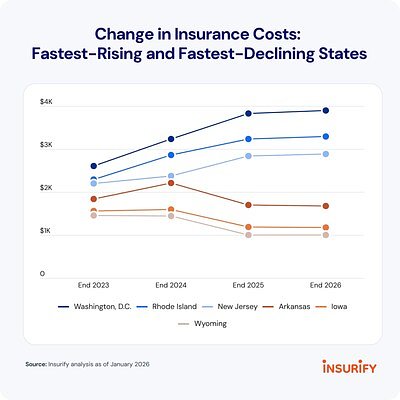

- Washington, D.C. Premium (2026): $4,088 (most expensive in the U.S.)

- Wyoming Premium (2026): $1,052 (30% decrease from 2025)

Experts agree that regional disparities in car insurance costs are driven by localized risk factors, higher repair costs, and macroeconomic pressures, creating a two-tiered affordability system where location is the primary determinant of premiums.

The Great Divide: Why Car Insurance Costs Are Soaring in Your State

CAMBRIDGE, Mass. – February 03, 2026 – While national headlines may suggest a cooling-off period for car insurance premiums, a starkly different reality is unfolding on the ground for millions of American drivers. A new report reveals a deepening chasm in auto insurance affordability across the United States, creating a two-tiered system where your zip code is becoming the single most significant factor in your annual bill.

According to the 2026 Insuring the American Driver Report from online insurance marketplace Insurify, national average full-coverage rates fell by 6% in 2025 to $2,144. However, this modest relief masks the dramatic 43% price hike drivers have endured since 2021 and obscures the extreme volatility at the state level. The report projects a slight 1% national increase in 2026, pushing the average to $2,158, but for drivers in already expensive states, the pain is set to intensify.

A Tale of Two Americas: The Growing Insurance Divide

The data paints a clear picture of a nation divided. While drivers in 39 states enjoyed falling or stable prices in 2025, those in ten other states and the nation's capital faced staggering increases. This trend highlights a growing affordability gap, where insurance is becoming cheaper in states where it was already inexpensive, and prohibitively expensive in areas with a high cost of living.

Nowhere is this disparity more evident than in Washington, D.C., which now holds the unenviable title of the most expensive place in the nation for car insurance. After an 18% surge last year, the average annual premium in D.C. hit $4,017. Projections for 2026 see that figure climbing even higher to $4,088.

Other states are not far behind. New Jersey saw its average premiums skyrocket by 20% in 2025, catapulting it from the 15th to the 6th most expensive state in the country with an average cost of $2,983. Michigan drivers also felt the squeeze, with a 12% jump pushing their average annual cost to $3,073, surpassing even notoriously high-cost states like New York. Rhode Island and Georgia also saw significant increases of 13% and 5%, respectively.

In stark contrast, drivers in Wyoming experienced a 30% decrease in their premiums, with the average annual cost for full coverage dropping to just $1,052. This vast gulf between Wyoming's affordable rates and D.C.'s soaring costs illustrates the powerful local forces now shaping the insurance landscape.

Behind the Rate Hikes: Risk, Repairs, and Regional Pressures

What is driving this extreme divergence? Insurers point to a confluence of macroeconomic headwinds and localized risk factors. The core principle of insurance is pricing for risk, and that risk is not distributed evenly across the country.

"Insurers have to respond to risk, and we're seeing those risks compounding in crowded states that already have a high cost of living," said Matt Brannon, Insurify's senior economic analyst and the report's author. "In places like New Jersey, more crashes and claims happen, repairs are more expensive, and insurers raise rates to keep up."

This analysis is supported by broader industry data. Densely populated urban areas inherently have higher traffic congestion, leading to a greater frequency of accidents. Furthermore, the cost to settle claims in these regions is higher due to elevated costs for labor, parts, and medical care.

Inflation remains a persistent driver of costs. While overall inflation may be moderating, the Consumer Price Index (CPI) for motor vehicle insurance has remained stubbornly high. This is fueled by the rising cost and complexity of vehicle repairs. Modern cars are packed with sophisticated sensors, cameras, and computer systems for features like advanced driver-assistance systems (ADAS). A minor fender-bender that once required a simple bumper replacement can now necessitate recalibrating multiple expensive sensors, dramatically increasing repair bills. Electric vehicles, with their specialized components and batteries, are also contributing to this trend, costing an average of 49% more to insure than their gasoline-powered counterparts.

Navigating the Maze: How to Lower Your Car Insurance Bill

The widening affordability gap is placing a significant financial strain on households, particularly in high-cost states where insurance can consume a substantial portion of a transportation budget. Even within cities, rates can vary dramatically by neighborhood, as seen in New York City, where a driver in the Bronx can pay more than double the premium of a driver in Queens.

While the trend of rising rates in certain areas may seem daunting, consumers are not powerless. Experts stress that proactive management of your insurance policy can lead to significant savings. The single most effective strategy is to shop around.

Drivers who remain with the same carrier for years often miss out on more competitive pricing. Using online comparison tools or working with an independent agent allows you to compare real-time quotes from multiple providers, potentially uncovering hundreds of dollars in annual savings.

Beyond comparing carriers, consider these strategies:

- Review Your Coverage: As your car ages, the value of comprehensive and collision coverage diminishes. You might save money by increasing your deductible or, for older vehicles, dropping these coverages altogether.

- Leverage Your Driving Record: A clean record free of accidents and violations is your best asset. Many insurers offer telematics programs that track driving habits via a smartphone app or plug-in device, rewarding safe drivers with substantial discounts.

- Hunt for Discounts: Insurers offer a vast array of discounts that often go unclaimed. Ask your provider about potential savings for bundling auto with home or renters insurance, being a good student, having anti-theft devices, or belonging to certain professional organizations.

- Mind Your Credit: In most states, insurers use a credit-based insurance score to help set rates. Maintaining good credit can have a direct, positive impact on your premium.

By taking a proactive approach and regularly reviewing their policies, drivers can gain more control over their insurance costs, even in a challenging market.