- 0.6% increase in public construction expenditures (Jan 2026, U.S. Census Bureau)

- 1.4% drop in home improvement spending (Jan 2026)

- 20.7% rise in steel mill products prices (Feb 2026, year-over-year)

Experts agree the construction industry is stabilizing but facing a bifurcated market where infrastructure and tech sectors thrive while traditional building segments decline, requiring strategic adaptation rather than a return to pre-pandemic norms.

Construction's New Normal: A Tale of Two Markets in 2026

By Charles Rivera

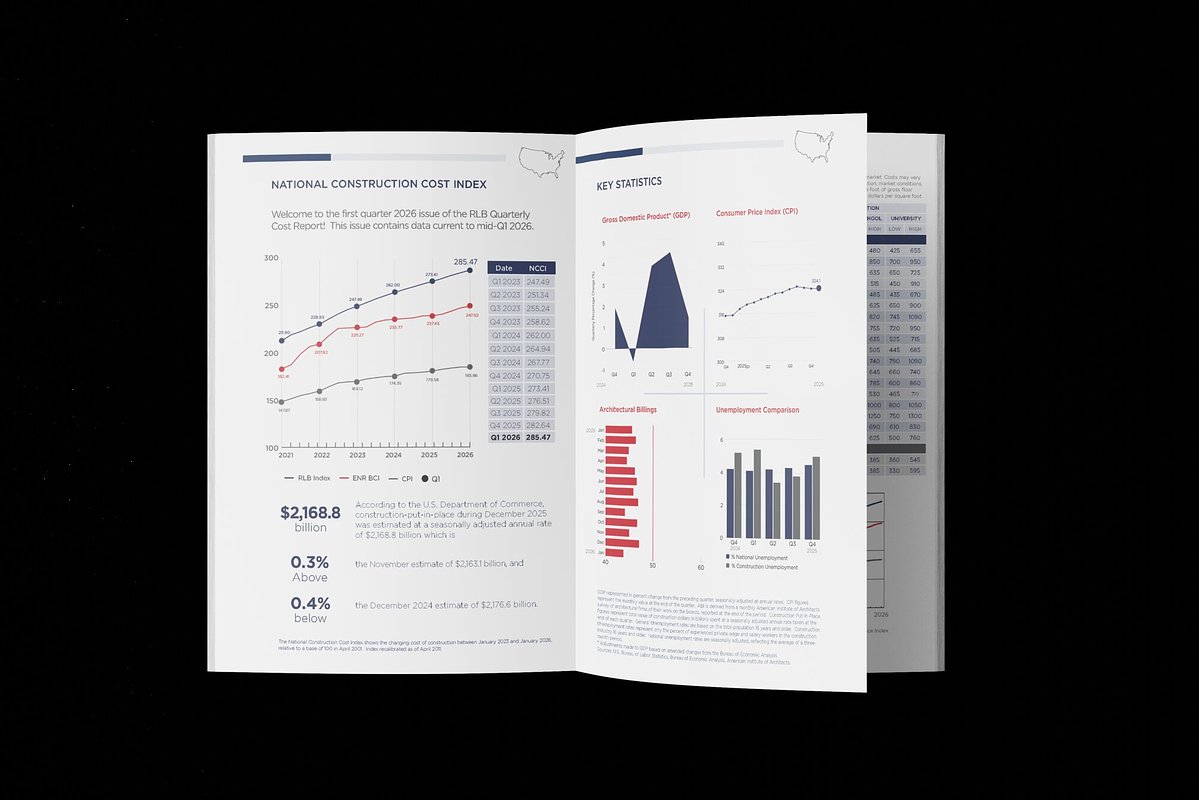

PHOENIX, AZ – March 24, 2026 – The North American construction industry is entering a period of recalibration, with a new report from global consultancy Rider Levett Bucknall (RLB) declaring an end to the extreme volatility of recent years. The firm's Q1 2026 Quarterly Cost Report suggests that stabilizing cost inflation is allowing developers to plan complex projects with greater confidence. However, a deeper look at market data reveals a landscape that is less about uniform recovery and more about a profound divergence, creating a tale of two distinct markets.

While predictability is returning, it is within an environment of subdued overall growth. One sector is fueled by massive public infrastructure spending and an insatiable demand for data centers and advanced manufacturing. The other sees traditional private commercial and residential projects cooling under the weight of high borrowing costs and shifting economic priorities. For industry players, navigating 2026 is not about a return to business as usual, but about adapting to this complex and bifurcated "new normal."

A Shift from Reaction to Refinement

According to RLB, the industry is transitioning from short-term, reactive decision-making into a phase of strategic refinement. “What we’re seeing now is the industry moving away from reactive decision-making and into a period of refinement,” said Paul Brussow, President of RLB North America, in the report's release. “The consistency in cost data we’re seeing allows for a level of planning that was difficult to achieve in previous years.”

This sentiment is partially supported by upstream indicators. The Architecture Billings Index (ABI), a key predictor of nonresidential construction activity nine to twelve months out, showed signs of bottoming out in February 2026. After months of decline, the index score rose to 49.4, indicating a slower pace of contraction. While still below the 50-point threshold for growth, the data suggests that owners and developers are using this period to reset project scopes and schedules, aligning new starts with current economic realities.

However, other forecasters urge caution. One associate director of forecasting at a leading construction data firm described the outlook for 2026 as one defined by "caution" and "subdued growth," with overall activity stabilizing at "relatively flat levels." This suggests that the "stabilization" is less about a surge in new work and more about a manageable, if modest, project pipeline that allows for more disciplined planning. The lesson for the market, as Brussow noted, is "not to retreat, but to refine."

The Great Divide: Infrastructure and Tech vs. Traditional Building

The most striking feature of the 2026 construction market is its stark division. A boom in public works and specific high-tech sectors is masking significant softness elsewhere.

On one hand, public construction is a powerful engine of growth. U.S. Census Bureau data from January 2026 showed a 0.6% increase in public construction expenditures, largely fueled by ongoing investment from the Bipartisan Infrastructure Law. Projects in electric power, utilities, and transportation infrastructure are filling order books, providing a reliable stream of work that counteracts weakness in other areas.

The private nonresidential sector is experiencing its own internal split. While overall spending in this category saw a slight 0.4% decline in January, this figure obscures explosive growth in niche markets. The demand for data centers, advanced manufacturing facilities, and power generation projects is unprecedented, with some large contractors reporting full pipelines into 2027. According to one market report, data centers alone now account for over a quarter of all nonresidential building construction in some key markets.

On the other side of the divide, traditional construction segments are struggling. The RLB report’s suggestion of a "resurgence in residential renovation" is contradicted by recent data, which showed a 1.4% drop in home improvement spending in January. The broader residential market continues to face headwinds from high mortgage rates and affordability challenges, with both single-family and multifamily construction starts declining. Similarly, traditional private nonresidential sectors like retail, office, healthcare, and education are experiencing a significant slowdown, with starts for healthcare and education projects down 39% and 18% respectively in the first quarter of 2026.

Navigating Persistent Headwinds

Even as parts of the market thrive, persistent cost pressures and supply chain challenges remain a critical concern for all sectors. The stabilization of cost inflation does not mean costs are decreasing; it means the rate of increase is more predictable. However, several key inputs continue to exert significant upward pressure on project budgets.

Tariffs on imported materials, particularly steel and aluminum, have become a structural component of construction costs. According to one chief economist for a major contractor association, a recent surge in construction input prices was driven primarily by "tariff-affected materials." Data from February 2026 showed iron and steel prices up 15.3% year-over-year, with steel mill products rising a staggering 20.7% over the same period. These policies, intended to protect domestic producers, allow them to raise prices, a cost ultimately borne by project owners.

Labor remains another major hurdle. The industry is grappling with a persistent shortage of skilled workers, forcing wages to rise faster than in the broader economy. One industry association estimates that an additional 349,000 new workers will be needed in 2026 just to keep pace with demand and replace a retiring workforce. This shortage not only drives up costs but also threatens to delay project schedules.

Furthermore, supply chains, while more resilient than in previous years, are far from normalized. Long lead times persist for critical electrical components like switchgear and transformers, stretching from 24 to 52 weeks. Volatility in global energy markets, with oil prices approaching $100 per barrel, is also poised to increase costs for fuel and transportation, adding another layer of complexity to long-range planning. Firms that succeed in this environment are those that, as RLB advises, emphasize productivity, adopt advanced procurement strategies, and lock in pricing early to mitigate these ongoing risks.