- The global commercial real estate market has narrowed its investor demand gap across property types to its tightest point in over three years.

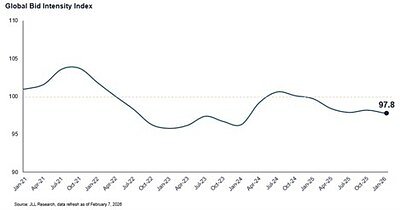

- JLL's Global Bid Intensity Index (BII) marked a significant turning point in July 2025, showing the first monthly improvement in bidder dynamics since late 2024.

- The office sector has shown marked improvement in bidding dynamics since its low point in late 2023.

Experts conclude that the global commercial real estate market is entering a phase of equilibrium with balanced investor demand across sectors, signaling a more normalized and predictable market for 2026.

The Great Convergence: Real Estate Bidding Balances Across Sectors

CHICAGO, IL – March 10, 2026 – The global commercial real estate market is entering a new phase of equilibrium, as the once-vast gap in investor demand across different property types has narrowed to its tightest point in over three years. According to a new report from global real estate services firm JLL, this convergence signals a more normalized, balanced, and potentially more predictable market for 2026, even as the supply of available properties for sale increases.

Analysis from JLL's Global Bid Intensity Index (BII), a proprietary tool that measures real-time investor competition, reveals that the bidding fervor for sectors like multi-family and industrial has moderated while interest in long-beleaguered office and retail properties has steadily climbed. This rebalancing act suggests a broadening of investor appetite and a return to fundamentals-based decision-making after years of volatility driven by interest rate shocks and pandemic-era disruptions.

A Market Finding Its Footing

The shift towards normalization is not a sudden development but the culmination of trends that gathered momentum in the latter half of 2025. JLL's index, which serves as a leading indicator for future capital flows, marked a significant turning point in July 2025, showing the first monthly improvement in bidder dynamics since late 2024. This stabilization was significantly bolstered by the Federal Reserve's decision to implement interest rate cuts in the fall of 2025, which provided a much-needed boost to investor confidence.

Despite a growing number of properties hitting the market, winning bids have remained highly competitive, preventing a sharp drop in overall market intensity. However, the market has seen a reduction in the number of extremely “hotly contested deals” that characterized previous peaks, leading to a slight flattening of the index’s growth curve entering 2026. This indicates a market that is active and healthy, but less frenetic and more rational than in recent years.

"While the current conflict in the Middle East introduces significant uncertainty, the global economy is better placed to absorb shocks than it has been in recent years—providing a meaningful buffer under a short-conflict scenario," said Richard Bloxam, CEO of Capital Markets at JLL. "The macro environment is supported by strong property sector fundamentals, more consensus around central banks, a settled interest rate policy and some decreases in macroeconomic volatility, all of which are giving investors continued confidence and renewed willingness to pursue investment opportunities."

A Tale of Four Sectors

The convergence story is most vividly told through the distinct yet increasingly connected performance of the four primary commercial real estate sectors. For years, investors flocked to a narrow set of asset classes, but 2026 is seeing a more democratic distribution of capital.

Multi-family: This sector continues to attract the most competitive bidding, backed by near-record levels of undeployed capital, often called “dry powder.” However, the sector is not immune to market pressures. Weaker rent growth in key markets, particularly in the United States, is forcing investors to be more disciplined in their underwriting, tempering the once-unbridled optimism.

Industrial & Logistics: After a period of explosive growth, bidding competitiveness for industrial assets rebounded strongly in the second half of 2025. The sector remains a darling for its ties to e-commerce and modern supply chains, but persistent uncertainty around global trade policies continues to be a key consideration for long-term investors.

Retail: The retail sector is experiencing a quiet renaissance. Liquidity is deepening for a wider variety of retail asset subtypes beyond grocery-anchored centers, and strong consumer spending has kept fundamentals solid. While the launch of more transactions has slightly softened the overall bidding intensity, the renewed interest marks a significant turnaround for the asset class.

Office: Perhaps the most compelling sign of market normalization is the recovery in the office sector. Bidding dynamics have shown marked improvement from the market’s low point in late 2023. This revival is being driven by two key factors: a growing pool of specialized bidders willing to invest in the asset class and, crucially, a greater number of lenders willing to quote on office loans. This signals that capital markets are beginning to differentiate between high-quality, well-located assets and the broader, challenged market, paving the way for a gradual recovery.

Navigating a Complex Global Landscape

The positive momentum in the commercial real estate market is unfolding against a complex backdrop of macroeconomic stability and geopolitical risk. The settled interest rate environment has been the single most important catalyst, allowing investors to price deals with greater certainty. This, combined with decreased macroeconomic volatility and resilient property fundamentals, has created a fertile ground for renewed investment activity.

Still, the geopolitical landscape, particularly the conflict in the Middle East, remains a significant source of potential market uncertainty. Investors are watching closely, weighing the resilience of the global economy against the potential for wider disruption.

"Even with more properties available for sale, investors are still competing just as fiercely. As demand grows more balanced across property types, we expect the healthy, active investment market will hold steady as buyer interest remains competitive and continues to diversify," Bloxam added. The data suggests that while external risks are present, the internal mechanics of the real estate market are healthier than they have been in years, pointing toward an intensifying capital markets liquidity cycle in 2026.

This broadening of investor interest across all major property types is fostering a more resilient and diversified marketplace, one that is less dependent on a few hot sectors and better positioned to navigate the opportunities and challenges of the year ahead.

Topics & Related

Capital Markets

Commercial Real Estate

Residential Real Estate

Corporate Finance

Related Company Pulse