- $80M–$100M: Fubo's projected Pro Forma Adjusted EBITDA for Fiscal 2026

- $300M+: Targeted Adjusted EBITDA by Fiscal 2028

- 99%: Wholesale fee agreement with Hulu + Live TV by 2028

Experts would likely conclude that Fubo’s merger with Hulu + Live TV has positioned the company for a strong financial turnaround, with predictable revenue streams and a clear path to profitability by 2027.

Fubo Charts Bold Path to Profit After Hulu + Live TV Merger

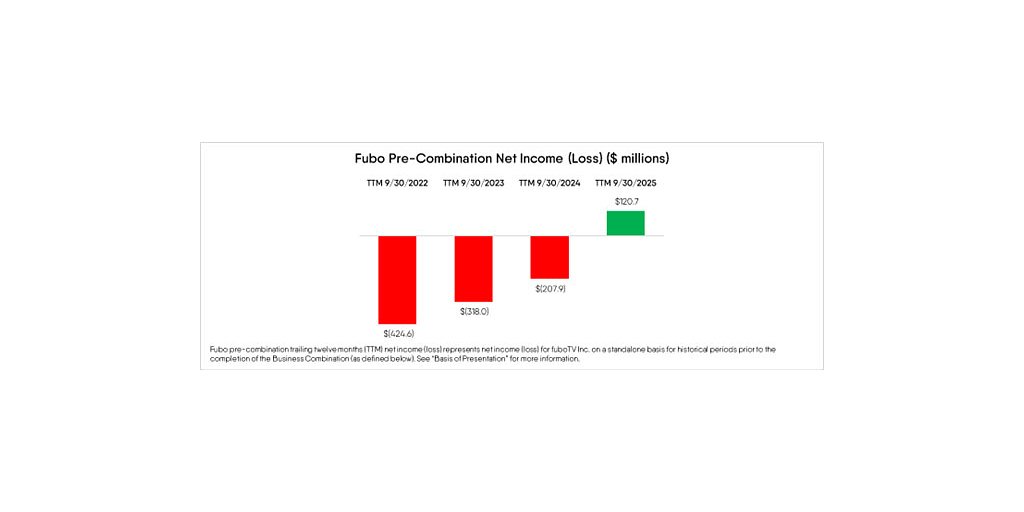

NEW YORK, NY – April 06, 2026 – FuboTV Inc. (NYSE: FUBO) today laid out an ambitious roadmap to profitability, signaling a strategic pivot from its long-held growth-at-all-costs mantra to a disciplined focus on financial stability. In a detailed letter to shareholders, the company projected significant earnings growth in the coming years, a direct result of its recent, transformative business combination with Disney’s Hulu + Live TV.

Fubo announced it expects to generate between $80 million and $100 million in Pro Forma Adjusted EBITDA in Fiscal 2026 and is targeting at least $300 million in Adjusted EBITDA by Fiscal 2028. Perhaps more significantly, the company projects it will achieve positive free cash flow starting in Fiscal 2027 and does not anticipate needing to raise additional capital through 2028. This represents a stark turnaround for a company that, like many in the streaming sector, has historically burned through cash to acquire subscribers in a fiercely competitive market.

“FuboTV Inc. is in the strongest financial position in our history based on our current outlook,” stated David Gandler, Co-founder and CEO, in his letter to shareholders. The new guidance is intended to provide investors with a clear line of sight into the company’s long-term earnings potential, which Gandler believes is not currently reflected in its stock price.

A New Financial Blueprint

The linchpin of Fubo’s confident forecast is the structural and financial synergy from its combination with Hulu + Live TV, which was completed in late 2025. The deal, which left The Walt Disney Company as the majority stakeholder of the combined entity, provides Fubo with a powerful and predictable revenue stream. A key component of this is a contractual wholesale fee agreement, where Fubo receives a growing percentage of Hulu + Live TV's carriage costs. This ratio is set at 95% in 2026, increases to 97.5% in 2027, and reaches 99% in 2028 and beyond.

This contractual step-up gives the company what it calls “strong visibility” into its earnings profile. This predictable income is a significant departure from the volatile economics of subscriber acquisition and retention alone. The projection of achieving an Adjusted EBITDA compound annual growth rate of over 80% between its 2026 and 2028 targets is built firmly on this foundation, alongside expected advertising synergies and cost optimizations.

The targets stand in sharp contrast to the company’s recent financial history. For Fiscal 2025, the combined entity posted a Pro Forma Net Loss of $(178) million, even while generating a positive Pro Forma Adjusted EBITDA of $59 million. The new guidance suggests the integration’s benefits are set to accelerate dramatically.

Navigating Market Skepticism

The confident financial forecast arrives as Fubo works to reshape its narrative on Wall Street, which has been skeptical of the company’s long-term viability. A recent reverse stock split, intended to lift the share price and attract institutional investors, was initially met with a sharp sell-off, a common reaction from markets that often interpret such moves as a sign of distress.

Gandler addressed this directly, framing the split as a “proactive, strategic decision” to broaden the potential investor base and not a precursor to dilutive equity raises. “Given our confidence in the strength of our financial position, we do not currently have any plans to do that,” he asserted. “We are operating from a position of financial strength.”

The new guidance appears to be having its intended effect, with some market analysts taking a more favorable view. The detailed multi-year plan provides the kind of clarity that fundamental investors seek, shifting the conversation from short-term trading dynamics to long-term operational performance and cash generation.

The Disney Deal and a Dual-Brand Strategy

Central to Fubo’s transformation is the business combination that created a new streaming powerhouse, now the sixth-largest pay TV provider in the U.S. with approximately 6.2 million subscribers. While Fubo’s management team, led by Gandler, operates the combined business, it’s a new structure where Disney holds a majority interest of around 70%.

Crucially, the Fubo service and Hulu + Live TV continue to operate as separate consumer-facing brands. This allows the company to pursue a dual-brand strategy that caters to different market segments. Hulu + Live TV offers a comprehensive entertainment-focused bundle, while the legacy Fubo service maintains its identity as a sports-first platform.

This structure also provides a strategic solution to a long-standing content gap. While the Fubo service itself still does not carry channels from NBCUniversal, the company can now market the more comprehensive Hulu + Live TV package to customers who desire that programming. “We have begun to market Hulu + Live TV to customers of the Fubo service who may prefer Hulu + Live TV’s more comprehensive channel line-up,” the company noted. This approach allows the combined entity to retain customers within its ecosystem while optimizing the channel lineups and unit economics of each individual service.

From Growth to Gains: A Maturing Strategy

The new financial discipline marks a coming-of-age for Fubo and reflects a broader trend across the streaming industry. The era of chasing subscriber growth at any cost is waning, replaced by a focus on sustainable profitability and average revenue per user (ARPU).

Gandler acknowledged this shift, stating, “While subscriber growth remains a key long-term driver of value, we are focused on pursuing that growth in an efficient and profitable manner. In the near term, this means prioritizing margin expansion and sustainable cash flow, which may result in periods of flat or modestly declining subscriber levels.”

This pivot is supported by the combined scale of the new entity, which provides greater leverage in negotiating content costs. As legacy content agreements for both Fubo and Hulu + Live TV come up for renewal, the company plans to align them to reflect its larger subscriber base, creating a path to structurally lower subscriber-related expenses.

The company’s financial house-cleaning extends to its balance sheet. Fubo has managed its debt to approximately $323 million, with no maturities until 2029. With a projection to end Fiscal 2026 with at least $200 million in cash and to achieve a net cash positive position by 2028, the company is sending a clear message that its days of relying on external financing are over. Gandler’s letter emphasized this point, stating the company has “enough cash to fund our business” and does not “anticipate needing additional outside financing through Fiscal 2028 based on our current operating plan,” a declaration aimed squarely at calming investor fears and signaling a new era of self-sufficiency.

Topics & Related

Funding & Investment

Merger

EBITDA

Fintech

Cloud & Infrastructure

Related Company Pulse