Chartwell's Strategic Shuffle: Reading the Signs in Seniors' Housing

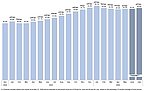

- Occupancy Rate: 95.2% in 2025, targeting 95% in 2026, up from a low of 76% in 2021.

- Portfolio Adjustment: 364 suites moved to 'repositioning' portfolio, despite 97.3% average occupancy.

- Distribution: Monthly payout of $0.052 per unit with a 3% DRIP bonus.

Experts would likely conclude that Chartwell's strategic repositioning of high-performing properties, combined with strong occupancy recovery and favorable market dynamics, signals confidence in long-term growth despite inherent risks.

Chartwell's Strategic Shuffle: Reading the Signs in Seniors' Housing

MISSISSAUGA, ON – June 15, 2026 – Chartwell Retirement Residences today announced a routine monthly cash distribution, but a closer look at the accompanying operational update reveals a far more compelling story about the company's long-term strategy and the bullish state of Canada's seniors' housing market. While the declaration of a $0.052 per unit payout provides a steady return for investors, it’s a subtle portfolio adjustment that offers the most significant insight into the operator's confidence and future direction.

Chartwell, one of the nation's largest seniors' housing providers, disclosed it is moving two high-performing properties into a 'repositioning' portfolio. This seemingly counterintuitive move, coupled with strong occupancy recovery and favorable market dynamics, warrants a deeper analysis for any investor looking to understand the future of this demographically-driven sector.

Payouts, Plans, and Investor Confidence

For unitholders, the immediate takeaway is stability and an attractive incentive for long-term ownership. The June cash distribution maintains the current payout level, reinforcing a sense of reliability. Furthermore, Chartwell continues to offer its Distribution Reinvestment Plan (DRIP), which sweetens the deal by granting bonus units equal to 3% of monthly distributions, allowing investors to compound their holdings commission-free.

This steady hand on distributions is more significant when viewed in its recent historical context. After navigating the pandemic without cutting its payout—a move described internally as a "difficult choice"—the company announced its first distribution increase since 2019 late last year. Management has signaled an intent to pursue annual increases as earnings grow, a clear vote of confidence in its operational and financial trajectory. This commitment is underpinned by a financial position that appears robust, with a debt-to-EBITDA ratio considered to be on the healthier, lower end of the Canadian REIT spectrum. For investors, this combination of a steady yield, a reinvestment bonus, and a stated growth ambition presents a compelling narrative of a company moving from post-pandemic recovery to a new phase of expansion.

Decoding the Occupancy Puzzle

The foundation of this confidence is built on a dramatic recovery in occupancy rates. While the press release points to forthcoming data for June and July, the trend lines have been exceptionally strong. After bottoming out near 76% in 2021, Chartwell's same-property portfolio saw a remarkable rebound, with one executive calling 2025 a "record year" as occupancy climbed 480 basis points to finish the year at 95.2%.

This momentum carried into 2026. Despite a seasonal dip attributed to a harsh winter and flu season, first-quarter results showed weighted average same property occupancy hitting 94.7%, a 400-basis-point improvement over the previous year. The company is now targeting a full-year average of 95%, a level that indicates operations are returning to, and in some cases exceeding, pre-pandemic norms.

This performance is not happening in a vacuum. It is a direct reflection of powerful market fundamentals. One senior source within the industry noted that the supply-demand imbalance has "never been as attractive as it is today." For nearly five years, new construction in the seniors' housing sector has been muted, creating a significant supply constraint. Simultaneously, Canada's aging demographics are fueling demand growth of 4-5% annually. This widening gap between a growing need and limited new inventory creates a powerful tailwind for established operators like Chartwell, enabling strong leasing activity and providing pricing power.

The Repositioning Gambit: A Proactive Strategy

Perhaps the most telling detail in today's announcement is the reclassification of two properties, comprising 364 suites, from the 'same property' portfolio to the 'repositioning' portfolio. Critically, these were not underperforming assets; they boasted an average occupancy of 97.3%.

Taking highly successful properties temporarily offline for 'repositioning' is a bold, forward-looking strategy. It signals that management is not merely content with high occupancy but is focused on maximizing the long-term value and revenue potential of its prime assets. Repositioning in the real estate sector typically involves significant capital investment for renovations, service model upgrades, or the introduction of new amenities. The goal is to elevate a property's market position, allowing it to command higher rents and attract a more discerning clientele upon its return to the active portfolio.

This move suggests Chartwell believes the market can support—and will reward—a higher-end product. By investing in already successful properties, the company is betting it can enhance their profitability well beyond current levels. For observers of 'The Nguyen Report', this is a classic success story signal: a market leader leveraging its strength to prepare for the next phase of growth, rather than simply managing the status quo. It aligns with the view that the Canadian senior living sector is at the beginning of a multi-year growth cycle, and Chartwell is positioning its assets to capture the maximum upside.

Balancing Opportunity with Inherent Risks

Chartwell’s optimism is palpable, both in its strategic moves and its forward-looking statements. The company is not just optimizing its existing portfolio; it is actively pursuing new growth with two construction projects underway in Quebec and another in development in Alberta, directly capitalizing on the supply-demand imbalance it has identified.

However, investors must balance this bullish outlook with the inherent risks detailed in the company's own regulatory filings. The forward-looking statements about occupancy and distributions are subject to a host of variables beyond management's control. Economic headwinds, shifts in government healthcare policy, rising labor costs, and increased competition all pose potential challenges. Furthermore, development and repositioning projects carry their own risks, including potential construction delays and cost overruns.

The current strategy appears to be a calculated and well-timed response to a uniquely favorable market. By strengthening its balance sheet, rewarding unitholders, and proactively reinvesting in its best assets, Chartwell is laying a foundation that aims to turn demographic inevitability into sustained financial growth.

📝 This article is still being updated

Are you a relevant expert who could contribute your opinion or insights to this article? We'd love to hear from you. We will give you full credit for your contribution.

Contribute Your Expertise →