- 3.8% year-over-year increase in Consumer Price Index (CPI) in April 2026

- Auto loan delinquencies at 3% (90 days or more past due)

- 3.8% year-over-year increase in used vehicle values (Manheim Used Vehicle Value Index, mid-May 2026)

Experts agree that auto refinancing has become a critical financial strategy for consumers to manage high-interest loans and improve cash flow amid persistent inflation and economic uncertainty.

Car Owners Find Relief as Auto Refinancing Becomes a Financial Lifeline

ENGLEWOOD, CO – May 22, 2026 – As American households navigate the complex economic currents of 2026, a powerful trend is emerging not on Wall Street, but in the family driveway. Faced with persistent inflation and borrowing costs that remain stubbornly high, consumers are increasingly turning to auto loan refinancing as a primary tool to reclaim financial flexibility and ease budgetary pressures. A new industry report highlights this shift, painting a picture of a nation proactively managing its debt rather than waiting for external economic relief.

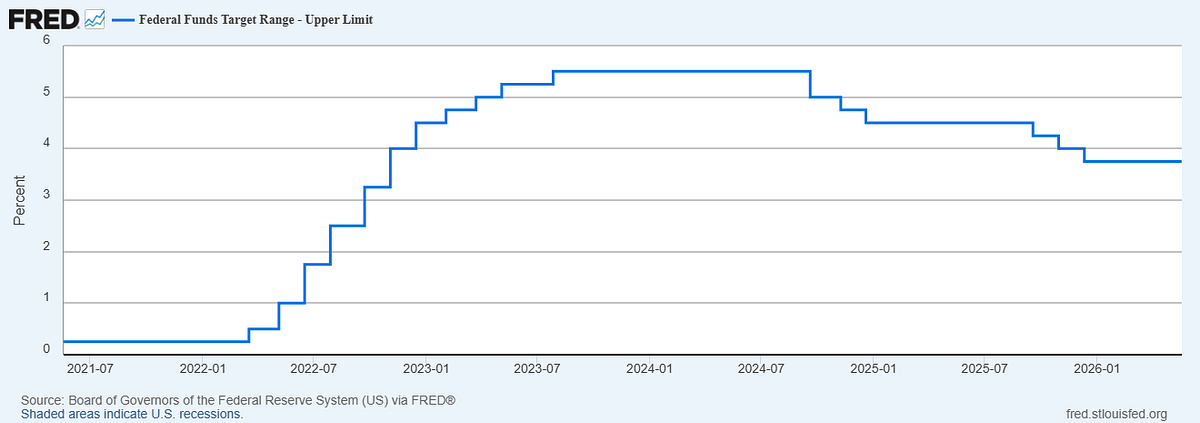

The Spring 2026 “State of the Auto Refinance Industry” report, released by automotive refinancing leader iLending, combines proprietary platform data with macroeconomic analysis to reveal a market defined by both challenge and opportunity. While the Federal Reserve has moved away from the aggressive rate hikes of previous years, the relief has been slow to trickle down, leaving millions of car owners locked into high-interest loans from the 2023-2025 period. This environment has transformed refinancing from a simple rate-shopping exercise into a critical strategy for improving monthly cash flow.

“Consumers are no longer waiting for relief, they’re creating it,” said Chad Nordhagen, VP of Marketing at iLending, in the company's release. “Refinancing is one of the fastest ways to improve cash flow without sacrificing mobility. In today’s environment, that matters more than ever.”

The Economic Squeeze on Drivers

The financial pressure detailed in the report is validated by broader economic indicators. Inflation, while moderating from its peak, continues to fluctuate and exert force on household budgets. According to the latest figures from the Bureau of Labor Statistics, the Consumer Price Index (CPI) rose 3.8% year-over-year in April, driven by significant increases in essential costs. Energy prices, for instance, have surged nearly 18% over the past year, directly impacting drivers at the pump, while shelter costs continue their steady climb.

Even with real GDP showing modest growth, this top-line number masks the financial strain felt by many families. The cumulative impact of years of inflation means that even with wage gains, purchasing power feels diminished. This reality is pushing consumers to scrutinize their existing financial obligations, with high-cost auto loans emerging as a prime target for optimization.

This climate of caution is also reflected in credit data. The Federal Reserve Bank of New York’s recent household debt reports show that while aggregate delinquency rates are stable, auto loan delinquencies remain elevated compared to historical norms. The flow of loans into serious delinquency (90 days or more past due) is hovering near 3%, with younger and sub-prime borrowers showing the most significant signs of payment stress. This underscores the urgency for many to find breathing room in their monthly budgets before credit issues escalate.

A Tale of Two Markets: Rates and Resale Value

The decision to refinance in 2026 is influenced by two key, and somewhat contradictory, market forces: interest rates and used vehicle values. The gap between the high rates attached to loans originated during the peak tightening cycle and the slightly softer rates available today continues to fuel strong refinance demand.

However, the opportunity is not just about securing a lower rate; it is increasingly about restructuring the loan for a more manageable monthly payment. For many, this provides immediate and tangible relief that can be redirected toward other rising costs.

Simultaneously, the used vehicle market has defied expectations of a steep price correction. According to the Manheim Used Vehicle Value Index, wholesale prices in mid-May 2026 were up 3.8% compared to the previous year. This unexpected resilience means that many car owners have maintained a favorable equity position in their vehicles, a critical component for a successful refinance.

“Vehicle values are behaving differently than many expected,” stated Nick Goraczkowski, President of iLending. “We’re seeing pockets of strength that are creating opportunity but also reinforcing how quickly conditions can change.”

This stability creates a time-sensitive window for borrowers. Strong vehicle equity can unlock better terms, but as the market continues to evolve in response to inventory levels and economic shifts, this advantage may narrow. External factors, such as the recent 47% spike in gas prices since late February, are also shaping the market, increasing demand and potential value for more fuel-efficient models.

Navigating Risk and Opportunity

In this environment, lenders have cautiously expanded their appetite, but underwriting standards remain disciplined. The most significant opportunities for refinancing are available to borrowers who can demonstrate a history of responsible payments and, ideally, an improved credit profile since they first took out their loan. Lenders are increasingly focused on credit quality and performance metrics to mitigate risk in a still-uncertain economy.

iLending’s report categorizes the opportunity as “strong” for near-prime and sub-prime borrowers who have improved their credit, and “moderate to strong” for prime borrowers who are primarily seeking payment flexibility. This highlights a key trend: refinancing is becoming a proactive financial health tool rather than a reactive measure taken in distress. By optimizing a major liability like a car loan, consumers can improve their debt-to-income ratio, potentially boost their credit score over time, and build a more resilient financial foundation.

The Digital Shift in Auto Finance

Underpinning the growth in refinancing is the continued evolution of financial technology. Today’s consumers expect a seamless, transparent, and efficient digital process, and the lending industry is racing to meet that demand. The friction-filled, paper-heavy loan processes of the past are being replaced by sophisticated online platforms.

Companies are investing heavily in their digital customer experience, offering tools like advanced prequalification that allow consumers to see potential savings without impacting their credit score. Streamlined applications, digital document submission, and personalized dashboards that provide clarity throughout the refinance journey are becoming industry standards. This technological shift is empowering consumers, giving them greater control and insight into one of their most significant financial decisions.

Looking ahead to the second half of 2026, the auto refinance market is expected to remain robust. The combination of persistent affordability pressures, a gradually improving rate environment, and increased consumer awareness points to continued demand. For millions of American households, the road to financial stability may well be paved by optimizing the loans on the vehicles sitting in their driveways.