- 76% of Americans carry debt, with 77% of borrowers saying it has held them back.

- 46% of debtors report that debt impacts their daily functioning.

- Household debt surpassed $17.5 trillion at the end of 2023, with credit card debt alone at $1.13 trillion.

Experts warn that chronic financial stress from debt is a significant public health issue, linked to higher rates of anxiety, depression, and impaired cognitive function.

America's Debt Crisis: 3 in 4 Are in Debt and Feeling the Weight

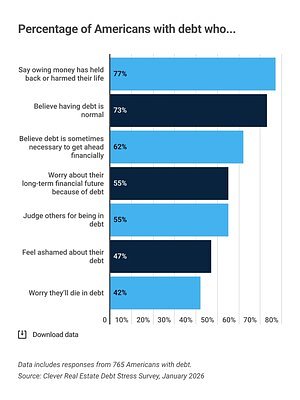

ST. LOUIS, MO – March 31, 2026 – A staggering three out of four Americans are currently carrying debt, and for the vast majority, it's more than just a number on a statement—it's a heavy burden that is actively harming their lives. A new report from real estate company Clever Real Estate paints a grim picture of the nation's financial health, revealing that 76% of Americans have some form of debt, with an overwhelming 77% of those borrowers stating it has held them back.

The findings underscore a pervasive and growing crisis of financial stress. Over half of those in debt (53%) report stressing about their finances at least once a week, a figure that jumps to nearly one in three (31%) who feel that anxiety every single day. This constant pressure is taking a measurable toll, with 46% saying it has impacted their daily functioning.

The Hidden Psychological Toll of a Nation in Debt

Beyond the balance sheets, the weight of debt is exacting a profound psychological price. The new data reveals a landscape of regret and anxiety, with nearly nine in ten debtors (87%) admitting they have regrets about their financial obligations. For many, this isn't a fleeting concern; 55% worry about their long-term financial future specifically because of the debt they hold, and a startling 42% are worried they will die in debt.

This sense of being trapped is exacerbated by a feeling of losing ground. In the past three months alone, 35% of Americans with non-mortgage debt saw their balances increase, more than double the number who managed to decrease their debt (15%). This aligns with national trends showing a steady rise in household debt, which surpassed $17.5 trillion at the end of 2023. Credit card balances, in particular, have swelled to over $1.13 trillion nationally, a reality reflected in the Clever report, which identifies credit card debt as the most common type (held by 44% of Americans), the most stressful (34%), and the most regretted (58%).

Experts in consumer psychology note that chronic financial stress is a significant public health issue. It is consistently linked to higher rates of anxiety, depression, and impaired cognitive function. The shame often associated with debt can create a debilitating cycle, preventing individuals from seeking help and leading to social isolation, which only worsens the mental health impact.

A Generational Chasm: The Debt Divide

The burden of debt is not shared equally across generations, creating a widening chasm in financial well-being. According to the report, Millennials (ages 27-42) are the most likely to be in debt, with 82% of the generation carrying some form of it. This stands in contrast to Baby Boomers (67%), who are the least likely to be in debt.

This generational disparity is rooted in a confluence of economic challenges that have uniquely impacted younger Americans. Millennials entered the workforce in the shadow of the 2008 financial crisis and have since been saddled with unprecedented levels of student loan debt, which now stands at a national total of $1.6 trillion. This educational debt, combined with soaring housing costs and periods of wage stagnation, has significantly delayed traditional wealth-building milestones. National data shows that while Gen X carries the highest average total debt, Millennials are disproportionately burdened by student loans, which hinders their ability to save for retirement or a down payment on a home.

Meanwhile, Gen Z is entering an even more precarious financial landscape. While their overall debt levels are currently lower, they face a severe housing affordability crisis, with mortgage rates and home prices creating formidable barriers to entry. The result is a growing gap in wealth and security, where younger generations are forced to take on more debt simply to achieve the same standard of living their parents enjoyed.

An Economic Tightrope Walk

The rising tide of personal debt is not occurring in a vacuum. It is a direct consequence of a challenging macroeconomic environment. Persistent inflation over the past few years, particularly in essential categories like food and shelter, has eroded the purchasing power of American households. While wage growth has occurred, it has often failed to keep pace with the climbing cost of living.

In response to inflation, the Federal Reserve's series of interest rate hikes has made borrowing significantly more expensive. Higher rates on credit cards, auto loans, and mortgages mean that existing debts become harder to pay down, and new debt comes at a much steeper price. For many families, credit cards have transitioned from a convenience to a necessity, used to bridge the gap between income and expenses. This is reflected in rising delinquency rates, especially for credit card and auto loans, which have been climbing steadily, with younger borrowers showing the most significant signs of distress.

The difficulty of escaping this cycle is profound. The report found that for 63% of those in debt, the last time they were free of non-mortgage debt was 2020 or earlier, and for more than a third (34%), it has been a decade or longer.

The American Paradox: Normal, Necessary, and Deeply Stigmatized

Perhaps the most telling finding is the deep contradiction in how Americans perceive debt. A majority of those in debt (73%) consider it to be a normal part of life, and 62% believe it's sometimes a necessary tool for getting ahead financially. This is particularly true for mortgages, which 43% of respondents view as the 'smartest' form of debt.

Yet, this acceptance coexists with a powerful undercurrent of shame and social judgment. Nearly half of debtors (47%) feel ashamed about their financial situation. This internal conflict extends to external judgment, as 55% of those with debt admit they judge others for being in debt.

This stigma has tangible consequences for personal relationships. The report reveals a striking reluctance to mix finances with love, as nearly two-thirds of Americans with debt (64%), and an even higher 71% of those without, say they would not marry someone with significant debt. This creates a silent struggle for millions who navigate a financial landscape where borrowing is often unavoidable, yet admitting to it remains a powerful social taboo.

Topics & Related

Geopolitics & Trade

Earnings & Reporting

Financial Performance

Interest Rates

E-Commerce

Related Company Pulse