Alpha Modus’s Fintech Gambit: Reading the Signals Behind Its Unbanked Play

- 1.3 million households in Kentucky and Pennsylvania are unbanked or underbanked, representing a significant market opportunity.

- $8 fee charged by Walmart for cashing checks over $1,000, highlighting the cost savings of Alpha Cash's service.

- 5% fee by PayPal's partner Ingo Money for instant check access, contrasting with Alpha Cash's fee-free model.

Experts would likely conclude that Alpha Modus's expansion into financial services is a strategic move to leverage its AI capabilities, enhance data insights, and create a scalable ecosystem that bridges retail and finance, while addressing a critical need for financial inclusion.

Alpha Modus’s Fintech Gambit: Reading the Signals Behind Its Unbanked Play

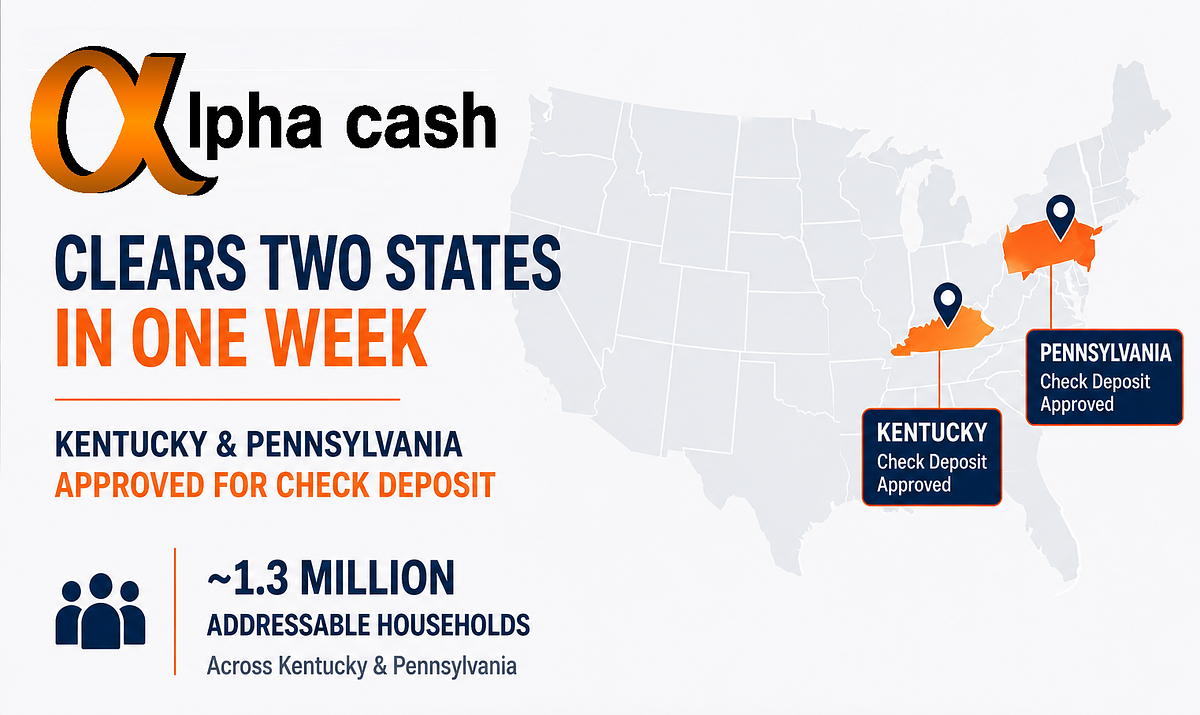

CORNELIUS, NC – June 09, 2026 – On the surface, the news is a straightforward fintech win: Alpha Modus Holdings, Inc. (NASDAQ: AMOD) announced it has secured regulatory clearance for its Alpha Cash mobile app to offer check deposits in Kentucky and Pennsylvania. For a company methodically pursuing a state-by-state rollout, clearing two states in a single week is a significant acceleration. The press release rightly frames this as a victory for financial inclusion, opening up modern banking services to over a million unbanked and underbanked households.

But to view this solely through the lens of a fintech app expanding its footprint is to miss the deeper strategic current. Alpha Modus is not a bank or a traditional financial services company. It is a vertical AI company whose patented technology is built to analyze in-store shopper behavior in real time. The move into financial services isn't a pivot away from its core identity; it's a calculated expansion of it. The real story here is not just about cashing checks, but about the convergence of retail media, artificial intelligence, and financial access—a maneuver that signals a far greater ambition.

The Unseen Market: Banking on Financial Inclusion

To understand the immediate impact, one must look at the landscape Alpha Cash is entering. Kentucky and Pennsylvania have a combined 1.3 million households that are either unbanked (no checking or savings account) or underbanked (relying on alternative services like payday lenders or check cashers). With poverty rates of 16.4% and 12% respectively, these are not abstract statistics; they represent working families for whom a traditional bank account is often out of reach due to minimum balance requirements, overdraft fees, or lack of physical branch access.

For this demographic, depositing a paycheck is a logistical and financial hurdle. It often means a trip to a check-cashing store that charges hefty fees—Walmart, for example, charges up to $8 for a check over $1,000. While digital competitors like PayPal and Chime offer mobile deposit, they come with their own complexities. PayPal, through its partner Ingo Money, can charge up to 5% for instant access to funds on certain checks. Others, like Green Dot, have eligibility requirements tied to direct deposit history. Alpha Cash aims to slice through this friction by offering a mobile-first solution.

“For consumers in these states who’ve had limited options to deposit a check without a traditional bank account, this is a real change,” said Chris Chumas, Chief Strategy Officer of Alpha Modus, in the company’s announcement. The statement underscores a genuine market need. By providing a reloadable prepaid debit card, free peer-to-peer transfers, and now state-approved check deposit, the app provides the foundational tools of modern banking without the traditional barriers, a move that could genuinely improve financial stability for hundreds of thousands.

The Compliance Gauntlet: A Blueprint for Expansion

Chumas also noted that “Getting check deposit right is harder than people realize.” This is a telling admission of the immense regulatory complexity that sinks many aspiring fintechs. Money transmission is governed by a patchwork of state-specific laws, creating a high bar for compliance. Instead of building a licensing infrastructure from the ground up in 50 different jurisdictions—a prohibitively expensive and time-consuming process—Alpha Modus has taken a more strategic route.

Its clearance in Kentucky and Pennsylvania was achieved under the “authorized delegate” framework, partnering with an established license holder, Barri Money Services, LLC. This model is a well-worn path for non-bank financial firms. It allows Alpha Modus to leverage Barri’s existing licenses to operate legally, while focusing its own resources on technology and user experience. The back-to-back approvals are not just a coincidence; they are a validation that this replicable model works. The company now has a proven blueprint to accelerate its expansion into other states, turning a daunting regulatory challenge into a scalable operational process.

This methodical approach signals a mature and deliberate strategy. It suggests the company understands that in the world of financial services, trust and compliance are not features but the very foundation upon which the business is built. By successfully navigating the NMLS system, the company is broadcasting its competence and reliability to both regulators and potential users.

The Strategic Core: Connecting AI, Retail, and Finance

Herein lies the most critical part of the analysis. Why is a company that specializes in a “closed-loop” retail AI framework—one that helps brands measure the impact of in-store advertising—venturing into financial services? The answer is synergy. Alpha Cash is not a standalone product but a crucial component of a larger ecosystem the company is building.

Alpha Modus’s core business is about understanding the consumer at the point of purchase. Its technology, like the recently announced ARIA enterprise AI, is designed for physical retail environments. The company is also deploying AI-enabled kiosks in partnership with hardware provider Genmega. These kiosks are envisioned as physical hubs for both retail media and financial transactions—bill payments, money transfers, and, critically, check cashing.

This strategy creates a powerful feedback loop. The retail presence provides a physical on-ramp for Alpha Cash users, particularly those who operate primarily in cash. In turn, the financial data generated by Alpha Cash users (while respecting privacy and security protocols) offers an invaluable, anonymized layer of insight into consumer spending habits. This data can enrich the company’s core AI models, making its retail analytics for brands and stores even more powerful. It’s a bold attempt to connect the digital ad a consumer sees, the way they manage their money, and the final transaction at the cash register.

This diversification is also a matter of strategic necessity. Public filings have noted an auditor’s doubt about the company’s ability to continue as a going concern, a challenge for many small-cap tech firms. By opening up a massive new addressable market in financial services, Alpha Modus is creating a vital new revenue stream beyond its patent licensing and AI software, signaling to investors a clear path toward sustainable growth.

Building a Digital-First Trust Economy

For this entire vision to work, Alpha Modus must win the trust of a demographic that is often rightfully wary of financial institutions. The company appears to understand this, emphasizing robust security and compliance measures. Its onboarding process includes stringent Know Your Customer (KYC) and Anti-Money Laundering (AML) checks, adhering to the same federal regulations as major banks. The app includes features like the ability to freeze a lost card, and its privacy policy details the safeguards in place to protect user information.

The combination of a secure, intuitive mobile app and a planned network of physical kiosks addresses the dual needs of its target users: digital convenience and the option for in-person interaction. This hybrid model could be the key to bridging the trust gap. The recent clearances in Kentucky and Pennsylvania are more than just new markets on a map; they are the first foundational pillars of a far more ambitious structure, one that aims to redefine the intersection of retail and finance. The underlying signal is one of confidence—not just in an app, but in a future where data flows seamlessly between a consumer's wallet and the modern marketplace.