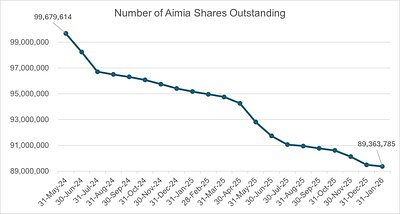

- 9 million shares repurchased: Aimia has bought back and cancelled over 9 million common shares since June 2024.

- 50% of NCIB completed: The current phase of the Normal Course Issuer Bid (NCIB) is nearly 50% complete, with 2.9 million of the 5.9 million shares authorized for 2025 repurchased.

- 30% upside potential: Analysts' average price target of C$4.00 suggests a potential upside of more than 30% from the current trading price of around C$3.02.

Experts view Aimia's aggressive buyback strategy as a direct response to its undervaluation, with cautious optimism driven by recent profitability and strong cash flow, though some remain wary due to mixed valuation metrics and structural challenges as a conglomerate.

Aimia's Buyback Bet: Closing the Value Gap on a Conglomerate

TORONTO, ON – February 02, 2026 – Aimia Inc. is continuing its aggressive push to realign its market valuation with its internal assessment, announcing another round of share repurchases as part of a multi-year campaign to enhance shareholder value. The company's latest move underscores a firm belief from management that its stock remains significantly undervalued, a common affliction for diversified holding companies.

In a press release issued today, the Toronto-based conglomerate (TSX: AIM) confirmed it had repurchased and cancelled 136,300 of its common shares during January 2026. While representing a modest 0.2% of its outstanding shares, the action is a consistent continuation of its Normal Course Issuer Bid (NCIB) program, a core pillar of its capital allocation strategy.

A Strategy to Close the Gap

The January buybacks, executed at a weighted-average price of $2.92 per share for a total of nearly $400,000, are just the latest chapter in a long-running initiative. Since first launching the program in June 2024, Aimia has now bought back and cancelled over 9 million common shares. The current phase of the NCIB, renewed in June 2025, is now nearly 50% complete, with the company having repurchased 2.9 million of the 5.9 million shares authorized for the year.

According to the company, the primary driver for the buybacks is a persistent disconnect between its share price and what it terms the "intrinsic value" of its net assets. "Aimia believes that the market price of its common shares may, from time to time, not reflect the intrinsic value of the company," it stated in the release, adding that repurchases represent an "appropriate and desirable use of the Company's funds."

This strategy is a direct signal to the market: management believes the best investment it can make right now is in its own stock. By reducing the total number of shares outstanding, the earnings and assets attributable to each remaining share increase, which can lead to a higher share price over time. This approach has been a consistent theme for Aimia as it navigates its post-loyalty program identity.

The Conglomerate Conundrum

Aimia's challenge is one familiar to many diversified holding companies. Its structure as a conglomerate, with core holdings in two distinct global businesses—Bozzetto, a sustainable specialty chemicals firm, and Cortland International, a ropes and netting solutions company—can make it difficult for the market to value accurately. Investors often apply a "conglomerate discount," penalizing companies that lack a single, clear focus, preferring to create their own diversification.

The company's aggressive buyback strategy is a direct assault on this discount. Rather than seeking out new acquisitions or major capital projects, Aimia is deploying its capital to shrink its own equity base. This raises a strategic question: does this reflect a strong conviction in the undervalued nature of its existing assets, Bozzetto and Cortland, or a lack of more compelling growth opportunities elsewhere?

For investors, the answer likely lies in the performance of those core businesses. In its most recent financial reporting, Aimia noted that both Bozzetto and Cortland showed resilience compared to their peers, despite facing softer demand and increased competition. The success of the buyback strategy is therefore intrinsically linked to the operational success and long-term value of these underlying companies. If they perform well, the buybacks will look like a shrewd move to acquire their earnings streams at a discount. If they falter, the capital could be seen as having been better deployed elsewhere.

Financial Fortitude and Renewed Profitability

Aimia's commitment to its buyback program is backed by newfound financial strength. The company's third-quarter 2025 results marked a significant turning point, delivering the first quarter of profitability attributable to equity holders since 2022. The company reported consolidated net earnings of $1.4 million, a stark improvement from a net loss of $2.2 million in the same period of the prior year.

This profitability was driven by strong operational performance, with consolidated adjusted EBITDA rising over 35% to $20.3 million. More importantly, the company's cash generation has improved dramatically. Net cash flow from operating activities surged to $15.1 million in the quarter, compared to just $1.3 million a year earlier. This financial health has been further bolstered by significant tax refunds from the Canada Revenue Agency, totaling over $38 million in the latter half of 2025.

With a cash and cash equivalents balance of $106.5 million as of September 30, 2025, Aimia has ample liquidity to continue its NCIB without compromising its financial flexibility. This strong balance sheet provides the necessary firepower to sustain the buyback strategy while also pursuing other strategic priorities, such as reducing holding company costs and efficiently utilizing its substantial tax loss carry-forwards, which stood at over $1 billion as of last spring.

Wall Street's Wary Optimism

The market and analyst community appear to be cautiously buying into Aimia's value proposition. The consensus among analysts covering the stock is a "Buy," with an average price target of C$4.00. This suggests a potential upside of more than 30% from its current trading price of around C$3.02, lending credence to the company's own claims of being undervalued.

However, the sentiment is not universally bullish. While its stock price has enjoyed a nearly 25% run-up over the past year, some valuation metrics remain challenging. The company's negative Price-to-Earnings (P/E) ratio, a result of past losses, makes traditional valuation difficult. Furthermore, some AI-driven analyses rate the stock as "Neutral," pointing to a mix of strong cash flow but pressured profitability and higher leverage.

This mixed view captures the essence of the investment thesis for Aimia. The company is in a transitional phase, executing a clear financial strategy to address a structural valuation problem. Recent operational improvements and a return to profitability are encouraging signs. The ongoing share repurchases serve as a constant, tangible expression of management's confidence, but investors are still watching to see if this financial engineering can translate into sustained, long-term value creation that finally closes the gap for good.

Topics & Related

Valuation & Market

EBITDA

Digital Transformation

Related Company Pulse