- Spot rates for dry vans: $2.41 per mile (up 9 cents from January 2026)

- Refrigerated rates: $2.88 per mile (up 7 cents from January 2026)

- Flatbed rates: $2.72 per mile (up 14 cents from January 2026)

- Diesel price: $4.859 per gallon (mid-March 2026, up from $3.71 in February 2026)

- Year-over-year spot rate increases: 18% to over 30% in certain lanes

Experts agree that the U.S. trucking industry is experiencing its tightest freight market in four years, driven by shrinking capacity, rising fuel costs, and external disruptions, signaling a structural shift away from the bargain-era pricing of recent years.

Trucking Rates Surge as Fuel Costs, Global Crises Roil Supply Chains

PORTLAND, OR – March 17, 2026 – The U.S. trucking industry is navigating a period of intense pressure as freight rates climb for the seventh consecutive month, driven by a tightening market, severe weather disruptions, and a dramatic spike in fuel costs linked to escalating global conflict. New data reveals a market rapidly shifting away from the overcapacity that defined recent years, signaling rising costs for shippers and, ultimately, consumers.

Data released by DAT Freight & Analytics for February 2026 shows a sustained rally in the spot market, where loads are booked for immediate transport. While overall monthly freight volumes saw a slight seasonal dip, the underlying trend points toward a significant tightening of available truck capacity.

The Anatomy of a Tightening Market

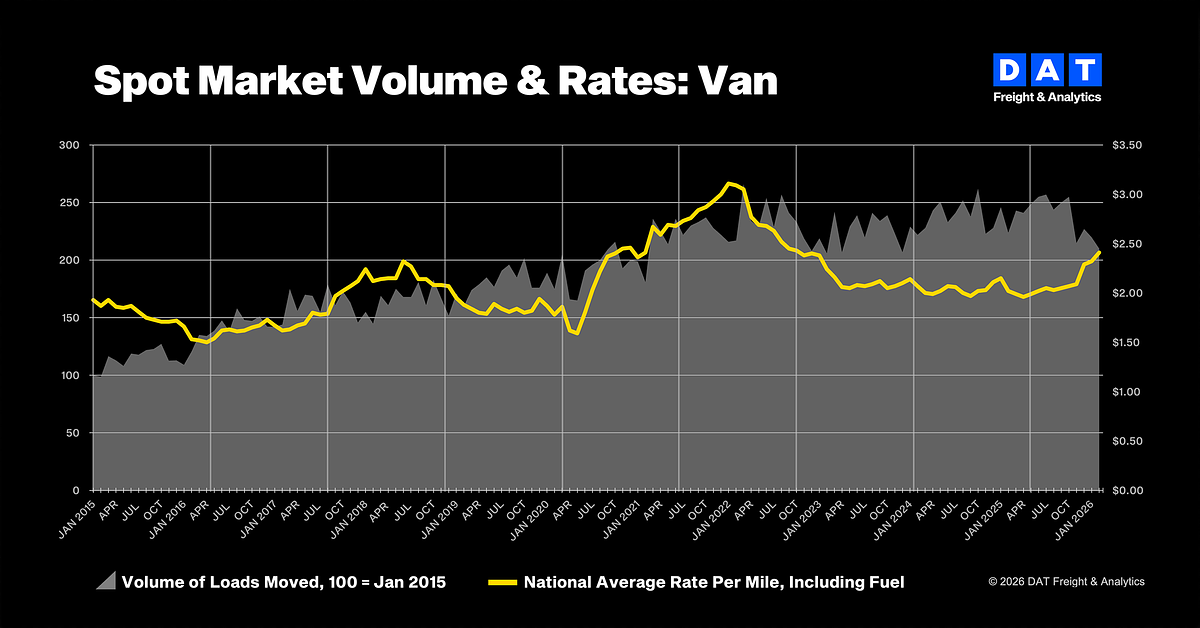

In February, national average spot rates for dry vans rose 9 cents to $2.41 per mile, while refrigerated (“reefer”) rates climbed 7 cents to $2.88 per mile. Both segments have now seen seven straight months of gains since August 2025, when they stood at just $2.03 and $2.41, respectively. Flatbed rates, often a barometer for the industrial economy, saw an even sharper monthly increase of 14 cents to $2.72 per mile.

According to DAT’s Truckload Volume Index (TVI), which measures monthly load volumes, van and reefer segments were down 5% and 7% compared to January. However, analysts note that these figures are misleading due to February’s shorter length. On a daily basis, freight activity for these segments actually increased, indicating firm demand.

Perhaps the most telling indicator of the market’s shift is the narrowing gap between spot rates and contract rates, which are pre-negotiated for longer terms. The spread between spot and contract van rates has shrunk to its smallest margin since March 2022. This convergence suggests that the excess truck capacity that has suppressed spot market pricing for nearly two years is evaporating, forcing spot rates to catch up to their contracted counterparts. Other market analyses confirm this trend, with some characterizing the current environment as the tightest freight market in four years, with year-over-year spot rate increases ranging from 18% to over 30% in certain lanes.

A Perfect Storm of Disruptions

The market’s rebalancing has been sharply accelerated by a confluence of external shocks. In February, a trio of severe winter storms—dubbed Fern, Gianna, and Ezra—paralyzed freight networks across the eastern United States. The storms took significant truckload capacity offline, causing spot load postings to surge by as much as 40% week-over-week in affected regions. Unlike previous weather events where a surplus of trucks allowed for a quick recovery, the market’s current lack of slack capacity meant disruptions lingered, amplifying the upward pressure on rates.

Simultaneously, escalating conflict in the Middle East has sent shockwaves through global energy markets. With the critical Strait of Hormuz shipping lane severely disrupted, the cost of transporting oil has skyrocketed. Brent crude, the international benchmark, has surged to nearly $103 per barrel, an increase of almost 50% since the conflict began in late February. This geopolitical volatility is directly translating to pain at the pump for the trucking industry.

The Fuel Factor: Squeezing Carrier Margins

While DAT reported the national average for on-highway diesel at $3.71 per gallon in February, the situation has since deteriorated dramatically. As of mid-March, the U.S. Energy Information Administration (EIA) reports the national average has soared to $4.859 per gallon, with prices in states like California exceeding $6.00. The EIA has sharply revised its 2026 forecast, now projecting an average diesel price of $4.12 for the year—a stark increase from its February prediction of $3.43.

Fuel represents the largest variable expense for trucking companies, often accounting for 30-40% of total operating costs. This rapid price surge places immense strain on carriers, particularly the small fleets and independent owner-operators that dominate the spot market. Unlike loads moving under contract, which typically include fuel surcharges that adjust with prices, spot rates are often negotiated as a single “all-in” price. This leaves carriers exposed to sudden spikes in diesel costs.

“Without fuel hedging, contract pricing, or surcharges, carriers will need to negotiate higher spot rates now to compensate for higher pump prices,” said Ken Adamo, DAT Chief of Analytics. “Otherwise, more carrier exits are likely—which, paradoxically, could accelerate the supply-side market recovery.”

This warning is already a reality. A slow but steady erosion of capacity has been underway for nearly two years, as thousands of trucking companies have exited the market, unable to withstand high operating costs and previously weak demand. This ongoing contraction, coupled with stricter regulatory enforcement and a slowdown in new truck manufacturing, is permanently removing capacity from the system.

An End to the Bargain Era

The convergence of rising rates, shrinking capacity, and spiking fuel costs marks a definitive end to what many shippers considered a “bargain era” for freight. The ripple effects are expected to travel throughout the U.S. economy. Economists are now warning that sustained high diesel prices will inevitably be passed down the supply chain, making everything from raw materials to finished consumer goods more expensive and adding to inflationary pressures.

In response to this new era of “predictable turbulence,” supply chain leaders are shifting their focus from pure cost-cutting to building resilience. Strategies like dual-sourcing materials, utilizing end-to-end visibility platforms, and exploring alternatives like intermodal rail are becoming critical. For businesses and consumers alike, the expectation of cheap, readily available shipping is being recalibrated to a new reality of structural volatility and persistently higher transportation costs.

Topics & Related

Transportation & Logistics

Related Company Pulse