- 62% of mortgage applicants experienced month-over-month income drops by mid-2025, up from 50% in early 2022.

- 65-percentage-point gap in home affordability between the most and least accessible states.

- Only 20% of workers in Food Preparation & Serving and 20% of Healthcare Support workers can qualify to buy a home in most states.

Experts agree that the mortgage system, designed for traditional salaried employment, is increasingly outdated and unfairly excludes workers with variable incomes, requiring urgent modernization to reflect today's labor market realities.

The Stability Gap: Is Your Paycheck Too Unpredictable to Buy a Home?

SAN FRANCISCO, CA – April 22, 2026 – For generations of Americans, the path to homeownership followed a familiar script: get a good job, save for a down payment, and secure a mortgage. A new, large-scale analysis suggests that script is being fundamentally rewritten. It’s no longer just about how much you earn, but how you earn it. Income stability has emerged as a formidable new gatekeeper, creating a “stability gap” that is locking millions of potential buyers out of the housing market.

A groundbreaking report by Truework, a platform specializing in income verification for lenders, reveals that the predictability of a person's earnings has become a decisive factor in mortgage qualification. The analysis, based on nearly 300,000 verified mortgage applicants from 2022 to 2025, shows a stark and growing divide between those with steady, salaried paychecks and the increasing number of Americans with variable or non-traditional incomes.

The Hidden Disqualifier

The report, titled “The American Dream, Recalculated,” exposes a dramatic rise in income volatility among aspiring homeowners. The share of mortgage applicants experiencing any month-over-month drop in income surged from 50% in early 2022 to 62% by mid-2025. More alarmingly, the severity of these income swings nearly tripled during the same period. This trend reflects the changing nature of the American workforce but clashes with the rigid architecture of mortgage underwriting.

“It is no longer enough to earn a good income; you need to earn it predictably, in the right occupation, and in the right state,” said Truework President and Founder, Ethan Winchell, in the report’s release. “For millions of Americans in service, care, and hourly roles, homeownership is increasingly out of reach, not because they aren't working hard enough, but because the system was not built to accommodate how they earn.”

This “stability gap” means that two individuals with the exact same annual income can have vastly different outcomes when applying for a loan. A salaried employee earning $80,000 a year may qualify with ease, while a freelance graphic designer or a commission-based salesperson earning the same amount over 12 months could be denied due to fluctuating monthly pay. Even modest income dips can be enough to push a borrower from qualifying to non-qualifying status.

A Divided Dream: The Lottery of Location and Livelihood

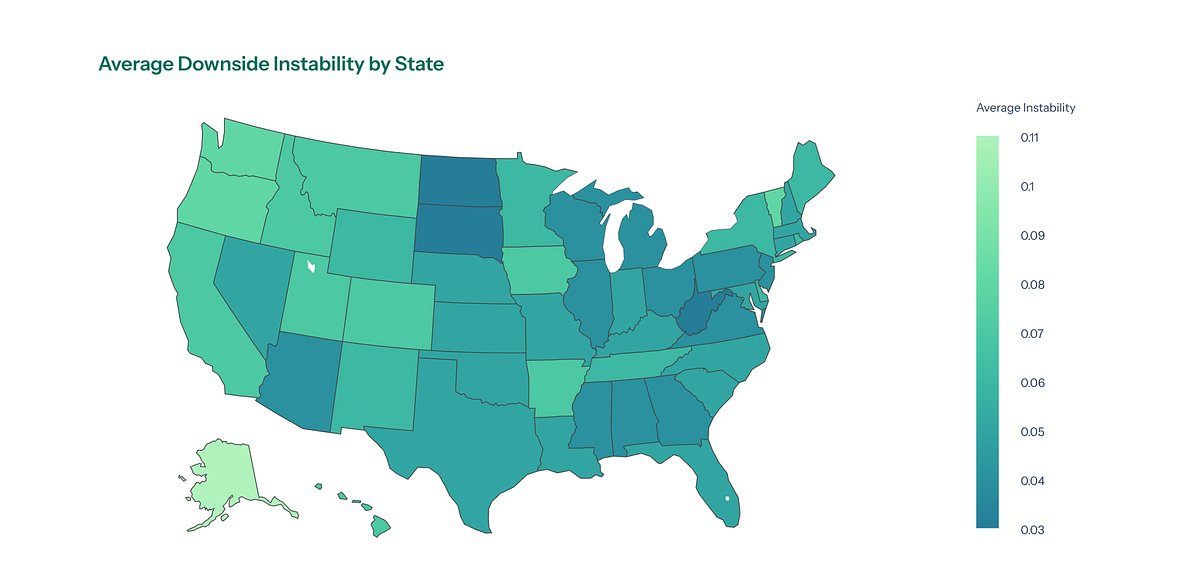

The analysis paints a picture of a deeply fragmented national housing market, where the dream of homeownership looks less like a unified goal and more like a geographic and occupational lottery. The report reveals a staggering 65-percentage-point gap in affordability between the most and least accessible states.

In high-cost states, the odds are daunting. In Hawaii, where the cost of living is nearly double the national average and a typical home exceeds $730,000, only 16% of verified borrowers meet standard mortgage eligibility criteria. The situation is similarly challenging in California (32% affordability) and Washington (40%).

Conversely, several states in the Midwest and South offer a much clearer path to ownership. In West Virginia, Louisiana, Illinois, North Dakota, and Ohio, affordability rates for applicants range from 76% to 81%. However, lower home prices do not automatically solve the problem. In many of these regions, the prevalence of hourly, seasonal, or commission-based work means that inconsistent income remains a significant barrier to financing, even with more attainable property values.

Profession plays an equally powerful role. Nationally, workers in salaried fields like Computer and Mathematical occupations (74% can afford to buy) and Management (71%) have a strong chance of qualifying for a mortgage. The outlook is grim for those in variable-income roles. Only 20% of workers in Food Preparation & Serving and about 20% of Healthcare Support workers can qualify to buy a home in most states. The contrast is even more extreme at the state level: nearly 100% of software engineers in Maine can afford a home there, while in Hawaii, a mere 4% of food service workers can say the same.

A System Built for a Bygone Era

The root of the issue lies in a mortgage qualification system designed for the post-war economy of steady, 9-to-5 employment. According to guidelines from government-sponsored enterprises like Fannie Mae and Freddie Mac, which back the majority of U.S. mortgages, variable income typically requires a 12- to 24-month history to be considered stable. Any declining trends in that income can lead to disqualification.

This framework is increasingly at odds with the modern labor market. While official definitions vary, data from the Bureau of Labor Statistics shows a significant portion of the workforce engaged in non-traditional work. In 2023, the BLS identified nearly 7 million contingent workers and almost 12 million independent contractors. These figures don't even fully capture the explosion of app-based gig work, a sector known for its income volatility.

As more Americans piece together a living through multiple jobs, freelance projects, and gig work, their income patterns naturally become more variable. Yet, the underwriting models used to assess their financial reliability have not kept pace, effectively penalizing them for the very flexibility that defines their work.

Can Technology Bridge the Gap?

The challenges highlighted by the Truework report are not going unnoticed. A new wave of financial technology (fintech) companies is developing solutions to provide a more nuanced and real-time picture of an applicant's financial health. By securely accessing and analyzing direct payroll and bank account data, companies like Plaid, Argyle, and Truework itself aim to automate and accelerate the verification process for all types of income, not just traditional W-2s.

These platforms can instantly verify employment and income from multiple sources, capturing a holistic view that is often missed by manual, employer-by-employer checks. For lenders, this technology promises faster, more accurate risk assessment. For borrowers with non-traditional income, it offers a chance to have their full earning potential properly evaluated.

The question remains whether the broader mortgage industry and its regulators will adapt. Without a systemic shift, the American Dream of homeownership may become a privilege reserved for those with the most predictable paychecks, leaving a growing segment of the workforce behind.

As Winchell warned, “Unless underwriting models evolve to better account for modern income patterns, we may end up with a housing market that systematically favors predictability over earning potential, leaving a growing share of the workforce on the outside looking in.”