- Median home sale price: $374,900 in January 2026, up 2.8% annually over the past two years

- Months of supply: Approximately four months of inventory, up from sub-two months during the pandemic

- Housing Affordability Index: 116.5 in January 2026, the highest since March 2022

Experts conclude that the U.S. housing market is stabilizing, with moderating price growth, improved inventory levels, and better affordability metrics creating a more balanced environment for buyers and sellers.

The Great Rebalancing: Housing Market Normalizes for Buyers in 2026

ARLINGTON, VA – February 12, 2026 – The U.S. housing market is showing clear signs of stabilization heading into the spring buying season, with key indicators suggesting a long-awaited return to a more balanced and sustainable environment for both buyers and sellers. A new report from online residential marketplace Homes.com reveals that while home prices continued their upward trajectory in January, the pace has moderated significantly, while improving affordability metrics are providing a tailwind for prospective homeowners.

Nationally, the median home sale price edged up to $374,900 in January 2026, a modest increase from $370,000 a year prior. This reflects an average annual price growth of just 2.8% over the past two years, a figure that closely mirrors overall inflation. More importantly for buyers, this slowdown in appreciation is occurring as incomes are growing more rapidly, chipping away at the affordability crisis that has defined the post-pandemic real estate landscape.

“The signs from the homes market are encouraging as we move into the spring homebuying season,” said Brad Case, Chief Residential Economist for Homes.com, in the report. “Home prices have continued to appreciate, but not at the breakneck speed that scared so many buyers away just a few years ago.”

A New Equilibrium for Buyers and Sellers

For years, the housing market has been characterized by fierce bidding wars, waived contingencies, and homes flying off the market in mere days. The latest data, however, paints a picture of a market finding its equilibrium. The inventory of homes for sale now stands at approximately four months of supply. While still below the six-month supply traditionally considered a perfectly balanced market, it represents a significant improvement from the sub-two-month supply seen at the height of the pandemic frenzy and is approaching pre-2020 norms.

This increase in available homes is giving buyers something they haven't had in years: time. The median number of days a home spent on the market before selling has stretched to nearly 12 weeks. This slowdown provides crucial breathing room for due diligence, securing financing, and thoughtful decision-making, a stark contrast to the high-pressure environment of the recent past. According to Homes.com, these metrics indicate that neither buyers nor sellers currently hold a definitive upper hand, setting the stage for more traditional negotiations.

This rebalancing is further supported by broader economic trends. According to the National Association of Realtors (NAR), its Housing Affordability Index rose to 116.5 in January, its highest level since March 2022. This improvement is a direct result of wage gains outpacing home price growth and mortgage rates that, while still elevated, have retreated from their recent peaks.

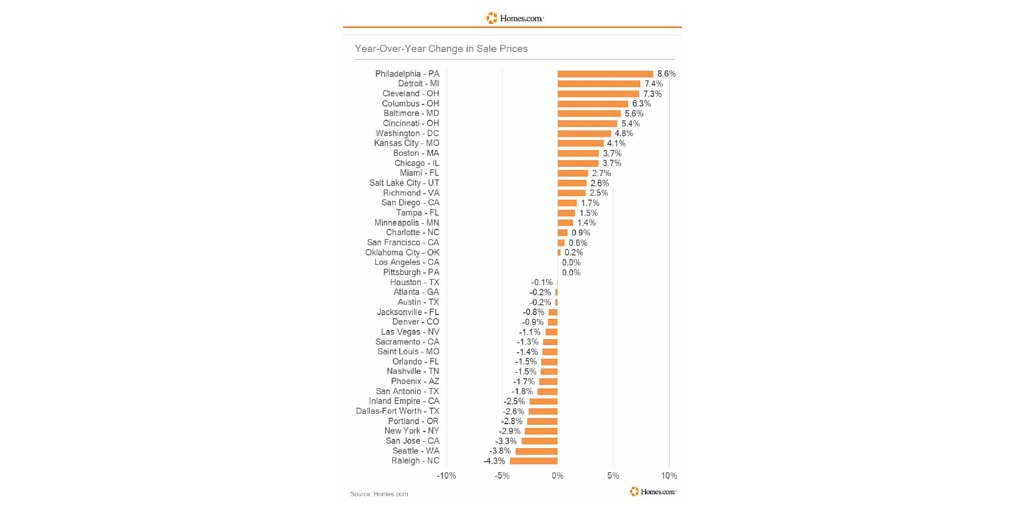

A Tale of Two Markets: The Great Regional Divide

Beneath the national trend of normalization lies a deeply fragmented market with stark regional disparities. The January report highlights a significant divergence between thriving markets in the Northeast and Midwest and cooling markets in parts of the South and West, many of which were epicenters of the pandemic housing boom.

Philadelphia has emerged as a national leader in price appreciation, with its median sale price surging 8.6% year-over-year to $380,000. Other cities followed a similar pattern, with strong growth in Baltimore (+5.6%), Washington D.C. (+4.8%), and Boston (+3.7%). The industrial Midwest also showed remarkable strength, with cities like Detroit, Cleveland, Columbus, and Cincinnati all posting annual growth exceeding 5%. This resilience is attributed to their relative affordability compared to other major metros and stable local economies.

In stark contrast, several cities that experienced supercharged growth during the pandemic are now undergoing a correction. The report noted price declines in southern and western cities, led by Raleigh, North Carolina (-4.3%) and Seattle (-3.8%). Other independent analyses confirm this trend, identifying Florida, Texas, and parts of the Mountain West as areas seeing the sharpest slowdowns. This cooling is largely seen as a necessary market correction, driven by a surge in inventory and a slowdown in the frantic in-migration patterns that pushed prices to unsustainable levels in 2021 and 2022.

The Affordability Equation: Modest Gains in a High-Cost World

While the narrative of improving affordability is a welcome one for buyers, experts caution that the journey back to pre-pandemic levels will be a long and gradual one. Despite recent gains, NAR data shows that housing affordability remains approximately 66% lower than the five-year average preceding the pandemic. The primary culprit remains the cost of financing.

Mortgage rates, which have a profound impact on a buyer's monthly payment and overall purchasing power, have settled in the low-to-mid 6% range. According to the Mortgage Bankers Association, the average 30-year fixed rate hovered around 6.2% in early February 2026. While this is a significant improvement from the near-8% rates seen in late 2024, the consensus among economists is that the era of dramatic rate drops is over. Most forecasts project rates will remain within the 6% to 7% range for the remainder of the year, suggesting that the current financing environment is the new normal.

This means that even with moderating prices and rising incomes, the financial hurdle to homeownership remains historically high. The combination of a higher price floor established over the last few years and mortgage rates double what they were in 2021 continues to challenge first-time buyers and those with limited down payments. The market's rebalancing may provide more opportunities, but it has not eliminated the significant financial barriers that persist.