Singapore's Green Hub Dream Clashes with Changi's Carbon Reality

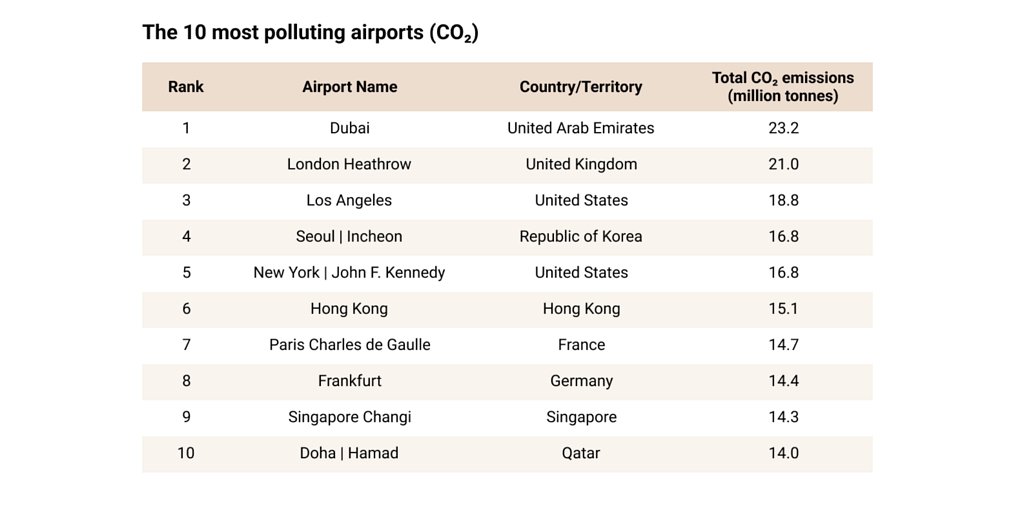

- 14.3 million tonnes of CO₂: Singapore Changi Airport's emissions in 2023, equivalent to 20 coal-fired power stations.

- 9th most carbon-intensive airport: Changi's global ranking in 2023.

- Less than 2.3% of airports: Have a credible net-zero plan for Scope 3 emissions.

Experts emphasize that while Changi Airport has proactive sustainability measures, its high carbon footprint highlights the urgent need for credible decarbonization pathways, particularly for Scope 3 emissions, to align with global climate goals.

Singapore's Green Hub Dream Clashes with Changi's Carbon Reality

SINGAPORE – May 15, 2026 – Singapore's carefully cultivated image as Asia's leader in green finance and sustainable aviation is facing a significant challenge from its own skies. A new report has identified Singapore Changi Airport, a jewel in the nation's economic crown, as the 9th most carbon-intensive airport in the world in 2023. The findings cast a shadow over the city-state's ambitious environmental goals, revealing a stark disconnect between aspiration and reality.

The report, titled the 2026 Airport Tracker and published by ODI Global and Transport & Environment (T&E), calculates that Changi Airport was responsible for 14.3 million tonnes of CO₂ last year. This staggering figure is equivalent to the annual emissions from more than 20 coal-fired power stations, placing the hub in an uncomfortable spotlight.

This revelation comes as Singapore aggressively positions itself to lead the region's transition to a low-carbon future, championing investments in sustainable aviation fuels (SAFs) and green financial instruments. However, the data suggests that the operational reality of its flagship airport is pulling in the opposite direction.

A Tale of Two Ambitions

The conflict between Singapore's environmental policy and its airport's carbon footprint underscores a global dilemma. The Airport Tracker, which draws on data from the International Council on Clean Transportation (ICCT), highlights that success for major aviation hubs is no longer measured solely by passenger numbers or connectivity.

"The race among global aviation hubs is no longer just about passenger volumes," stated Jude Lee, Regional Policy and Program Director for T&E's APAC division. "It is increasingly about who can demonstrate the most credible, MRV-backed decarbonisation pathway."

The report's methodology focuses heavily on Scope 3 emissions—the indirect emissions that constitute the vast majority of an airport's climate impact. These emissions, generated primarily by aircraft taking off and landing, as well as passenger and employee ground transport, account for over 90% of the total carbon footprint. While airports have direct control over their Scope 1 and 2 emissions from ground vehicles and purchased electricity, tackling Scope 3 requires influencing a complex ecosystem of airlines, service providers, and travelers.

This is where the industry's systemic failure becomes apparent. According to the Airport Tracker, fewer than 2.3% of the 1,300 airports surveyed have a credible net-zero plan for their Scope 3 emissions. This widespread lack of accountability is a critical barrier to aviation's decarbonization, especially as emissions continue to climb post-pandemic.

Changi's Proactive Defense

In the face of such criticism, Changi Airport Group (CAG) can point to a robust and proactive sustainability strategy. The airport operator has already committed to reducing its direct Scope 1 and 2 emissions by 20% by 2030 (from a 2018 baseline) and aspires to achieve net-zero by 2050. Its action plan is one of the most detailed in the region.

Central to this strategy is the adoption of Sustainable Aviation Fuel. Starting in 2026, Singapore will mandate a 1% SAF usage for all flights departing from Changi, with a goal to increase this to 3-5% by 2030. To fund this transition, a levy will be applied to tickets, directly passing the cost of decarbonization onto travelers. This move is supported by a local supply chain, with Neste's expanded refinery in Singapore capable of producing up to one million tonnes of SAF annually.

Beyond fuel, CAG is aggressively electrifying its ground operations. The goal is for all new light vehicles and tractors on the airside to be electric from 2025, with a full transition for all airside vehicles to cleaner energy by 2040. This is complemented by the installation of Singapore's largest single-site rooftop solar panel system, set for completion in 2025, to increase on-site renewable energy generation. While these measures are significant for tackling direct emissions, they only address a small fraction of the total emissions cited in the T&E report.

Asia-Pacific: The New Epicenter of Aviation Pollution

The report's findings extend far beyond Singapore, identifying the Asia-Pacific region as the new global leader in aviation emissions. The region now accounts for 32% of the world's aviation CO₂, surpassing North America and Europe. This surge is fueled by a burgeoning middle class, increased economic activity, and a rapid post-pandemic recovery in travel. In March 2024 alone, Asia-Pacific airlines saw a 37.5% year-on-year increase in international passengers.

This explosive growth has turned a handful of major hubs into massive sources of pollution. According to the report, just 100 airports worldwide are responsible for approximately two-thirds of all passenger flight emissions. As passenger numbers in Asia-Pacific are projected to double by 2043, the region's contribution to global emissions is set to grow even larger, making its decarbonization efforts a matter of global urgency.

"Since the Paris Agreement, aviation emissions have risen steadily while other sectors have begun to decarbonise," said Sam Pickard, a Research Associate at ODI Global. "A genuine strategy that includes demand management is sorely needed."

The Coming Carbon Bill

The era of unchecked aviation emissions appears to be drawing to a close, with regulatory and financial pressures mounting. The European Union is leading the charge, moving to phase out free carbon allowances for airlines and extend its Emissions Trading System (ETS) to cover all departing international flights. This policy alone could generate over €12.7 billion in annual revenue, creating a powerful financial incentive for airlines to decarbonize their operations.

This move by the EU sends a clear signal to the rest of the world: the cost of carbon will be priced into air travel. For hubs like Changi and airlines operating long-haul routes to Europe, this represents a significant future liability. The question is no longer if aviation emissions will carry a price, but when and how much that price will be.

While the UN's global offsetting scheme, CORSIA, aims to create a worldwide standard, the EU's more aggressive approach could set a de facto global benchmark, compelling other regions to follow suit or risk competitive disadvantages. As airports and airlines navigate this new reality, the strategies that once guaranteed success—rapid expansion and maximizing passenger volume—are being fundamentally re-evaluated. The focus is now shifting to resilience, sustainability, and the ability to operate within a carbon-constrained world.

📝 This article is still being updated

Are you a relevant expert who could contribute your opinion or insights to this article? We'd love to hear from you. We will give you full credit for your contribution.

Contribute Your Expertise →