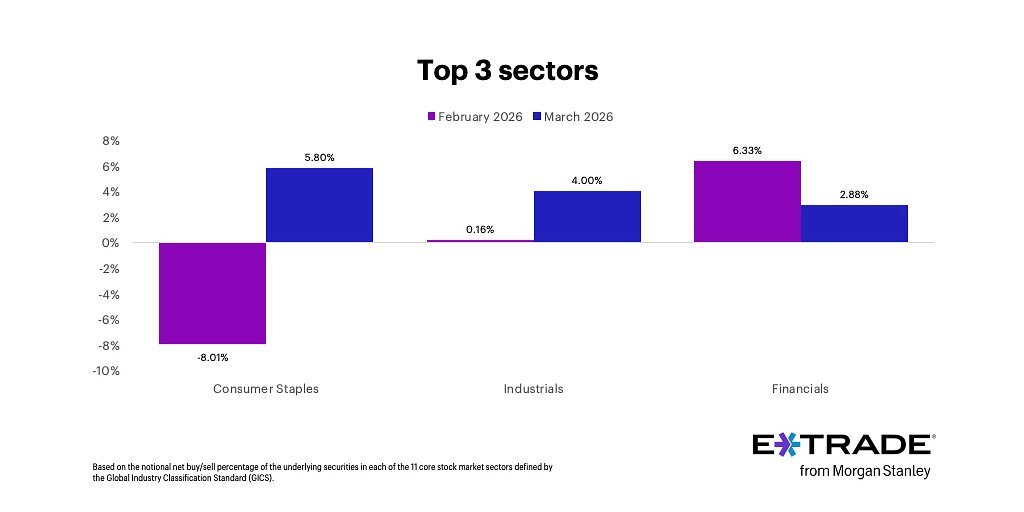

- Consumer Staples: +5.80% net buying activity

- Energy Sector: -8.86% net selling activity

- U.S. Inflation Rate: 2.4%

- U.S. Manufacturing PMI: 52.7 in March

Experts would likely conclude that retail investors are adopting a defensive strategy, prioritizing stability and value amid economic uncertainty and geopolitical risks.

Retail Investors Go Defensive, Flee Energy Amid War-Fueled Oil Spike

NEW YORK, NY – April 02, 2026 – In a market gripped by geopolitical turmoil and persistent inflation, retail investors are making decisive, and at times paradoxical, moves. A new monthly study from E*TRADE from Morgan Stanley reveals a significant flight to defensive sectors, while simultaneously showing a mass exit from the booming energy sector, even as oil prices skyrocket.

The report, which tracks the net buying and selling activity of retail clients across 11 major stock market sectors, shows that Consumer Staples (+5.80%), Industrials (+4%), and Financials (+2.88%) saw the highest net-buying activity in March. In stark contrast, investors heavily sold positions in Energy (-8.86%), Utilities (-2.14%), and Communication Services (-0.91%).

This rotation offers a fascinating glimpse into the mindset of the individual investor, who appears to be navigating a complex economic landscape by simultaneously bracing for a downturn and taking profits from the market’s most volatile corner. These moves come as the U.S. economy grapples with a 2.4% inflation rate, a steady Federal Reserve policy, and the profound economic shockwaves of the 2026 Iran war.

The Retail Playbook: A Flight to Perceived Safety

The surge of capital into Consumer Staples is a classic defensive maneuver. This sector, which includes companies that produce household necessities and food, tends to perform well during periods of economic uncertainty due to its stable demand. The move aligns with troubling signals from consumer sentiment surveys. While the Conference Board's Present Situation Index surged in March, reflecting satisfaction with current conditions, its Expectations Index—a measure of future outlook—continued its pessimistic slide, remaining below the critical 80-point threshold that often signals a coming recession.

This “schizophrenia” in consumer confidence, where the present feels secure but the future looks bleak, appears to be directly influencing investment decisions. By loading up on staples, retail investors are effectively stocking their portfolios for a potential economic storm.

Meanwhile, the strong net buying in the Industrials sector points to a belief in the tangible economy. This confidence is bolstered by hard data, including a U.S. Manufacturing PMI that climbed to 52.7 in March, indicating sustained recovery and growth in new orders and production. The trend suggests a bet on the resilience of American manufacturing, possibly fueled by ongoing “reshoring” efforts as companies move supply chains closer to home.

The buying in Financials suggests a more nuanced strategy. With the Federal Reserve holding interest rates steady at a range of 3.50%-3.75% but inflationary pressures mounting, some investors are likely betting on a “higher-for-longer” rate environment. Such a scenario can bolster the profit margins for banks and other financial institutions. For others, it may be a value play in a sector that has underperformed over the past year, presenting a potential buying opportunity.

The Great Energy Paradox: Selling Into a Boom

The most dramatic and telling data point from the E*TRADE study is the staggering 8.86% net selling in the Energy sector. This move is deeply counterintuitive on the surface. The month of March was defined by the Iran war and the closure of the Strait of Hormuz, a crisis that removed an estimated 20% of global oil supplies from the market and sent Brent and WTI crude prices soaring to nearly $112 a barrel.

In the face of what has been called the “largest supply disruption in the history of the global oil market,” retail investors didn't pile in; they cashed out. This behavior points to several possible psychological drivers. Many investors who held energy stocks likely saw the massive, war-driven price spike as a golden opportunity to take substantial profits off the table. After a volatile period for the sector, locking in gains may have seemed more prudent than gambling on further escalations.

Furthermore, the extreme volatility itself may have been a deterrent. With analysts floating potential oil prices ranging from $150 to $200 a barrel if the conflict worsens, the sector has become a hotbed of geopolitical risk. For the average retail investor, the complexity and unpredictability may outweigh the potential rewards. Selling the sector, even as it booms, represents a conscious decision to de-risk and step away from the epicenter of global tensions.

A Tale of Two Sentiments: Retail vs. Institutional Flows

Comparing the retail trends to institutional activity reveals a more complex market picture. Institutional investors were also net buyers of equities in March, suggesting a broad appetite for stocks. However, the details show diverging strategies. Weekly data from Bank of America indicated that while institutional and private clients were buying, hedge funds were net sellers, complicating any simple “smart money” versus “dumb money” narrative.

Institutions appeared to be focused on large-cap equities, a trend that aligns with retail’s interest in established Industrial and Financial names. However, the aggressive retail selling in Energy stands in contrast to the sector’s headline-grabbing performance, a move that may differ from institutional strategies focused on momentum or macroeconomic plays.

This divergence underscores that retail investors are an independent force, responding to the market with their own unique blend of data analysis, long-term strategy, and behavioral finance. Their collective actions are less a mirror of institutional flows and more a reflection of consumer-level economic anxieties and risk tolerance.

Reading the Market's Mixed Signals

Ultimately, the E*TRADE data paints a portrait of an investor base preparing for a difficult road ahead. The selling in Utilities, despite the sector's strong year-to-date performance, suggests a growing sensitivity to valuation, as analysts have flagged the sector as overvalued with historically low dividend yields.

Taken together, the rotation out of high-flying but risky Energy and expensive Utilities, and into defensive Staples and economically sensitive but potentially undervalued Industrials and Financials, marks a clear shift. It is a move away from the growth-oriented themes of recent years and toward a portfolio strategy built on value, tangible assets, and resilience.

As the second quarter of 2026 begins, the market remains on a knife's edge, balanced between a resilient U.S. economy and the looming threats of global conflict and renewed inflation. The actions of retail investors in March show they are not waiting passively for the outcome; they are actively repositioning their portfolios for a future they view with increasing caution.