- 2025 Profit Margin: Lloyd's syndicates achieved an 18.8% profit margin, significantly higher than the five-year (14.5%) and nine-year (7.9%) averages.

- Pre-Tax Profit: Lloyd's reported a £10.6 billion pre-tax profit for 2025.

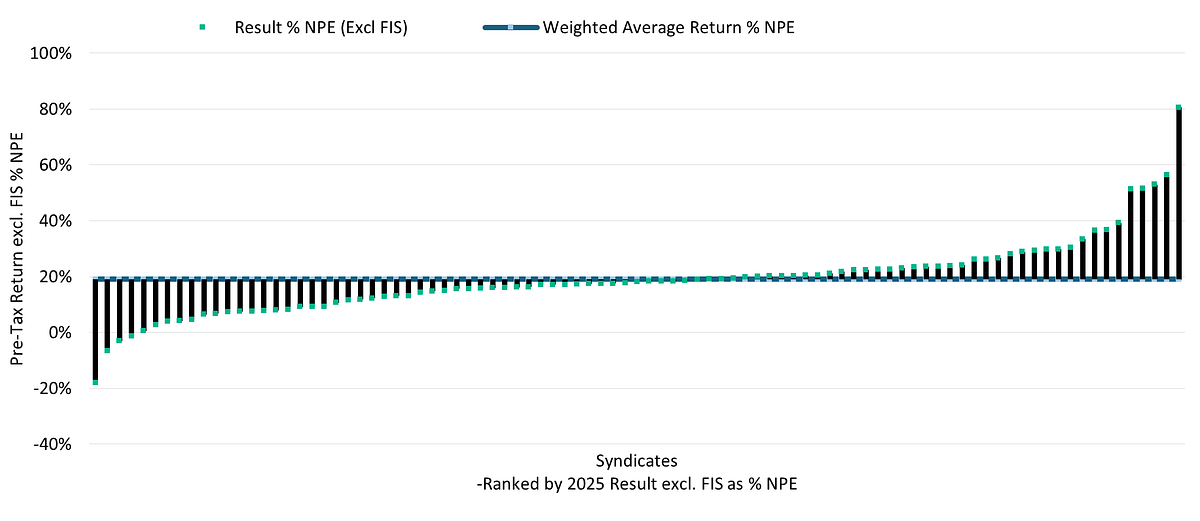

- Performance Gap: Top quartile syndicates averaged 32.1% profit, while the bottom quartile managed just 6.5%, a 25.6 percentage point difference.

Experts conclude that while Lloyd's 2025 results were strong overall, the market is deeply divided between high-performing established syndicates and struggling newer entrants, with future profitability increasingly dependent on disciplined underwriting as investment returns soften.

Lloyd's Strong 2025 Results Mask a Deepening Market Divide

LONDON, UK – April 23, 2026 – The Lloyd's of London market celebrated an exceptionally profitable year in 2025, with syndicates posting their best results in nearly a decade. However, beneath the impressive headline figures lies a starkly divided marketplace, where a chasm separates the high-flying top performers from a struggling contingent of newer entrants.

A new analysis by Syndicate Research Limited (SRL) reveals that the weighted average profit for Lloyd's syndicates in 2025 was a robust 18.8% of net premium earned, significantly outpacing the five-year average of 14.5% and the nine-year average of 7.9%. This performance, corroborated by Lloyd's own official report of a £10.6 billion pre-tax profit, was bolstered by strong investment income and a relatively calm year for major catastrophes. Yet, this aggregate success obscures a dramatic disparity at the individual level, with syndicate results ranging from a staggering 81% profit to a painful 18% loss.

A Tale of Two Tiers

The 2025 results paint a clear picture of what SRL describes as a "two-tier market." The top quartile of syndicates generated a weighted average profit of 32.1%, while the bottom quartile managed just 6.5%—a staggering 25.6 percentage point difference in a year with relatively low major losses. This performance gap is not a new phenomenon; over the past nine years, the top tier has consistently outperformed the bottom by an average of 13.8 percentage points.

A key factor in 2025's divergence was a comparatively benign U.S. hurricane season. This especially benefited syndicates specializing in Excess of Loss coverage, which dominated the top performance rankings. The weighted average profit for this peer group soared to 49%, more than double the market average. Topping the list was Syndicate 1176, a specialist in nuclear risk managed by Chaucer, which has a long history of generating substantial profits in years free of major incidents in its niche.

In stark contrast, the bottom of the league table was largely populated by recent market entrants. Of the five worst-performing syndicates, three only began trading in 2024, with another starting in 2023. This highlights a persistent challenge within the Lloyd's ecosystem, where maturity often dictates performance. Independent analysis has shown that mature syndicates historically outperform newer ones by a significant margin on key metrics like the combined ratio, a gap that widens considerably in years with heavy catastrophe losses. These newer ventures often face higher initial operating costs and capital requirements, creating an uphill battle from their inception.

Dual Engines of Profitability Face Headwinds

The market's strong 2025 performance was powered by two engines: disciplined underwriting and exceptional investment returns. Syndicates achieved an average combined ratio of 85.7%, a measure of underwriting profitability where a figure below 100% indicates a profit. This result is significantly better than the nine-year average of 96.2% and was heavily influenced by a major claims ratio that fell to 5.8%, nearly half the long-term average.

Alongside underwriting success, investment income provided a powerful tailwind. Returns averaged 7.7% of net premium earned, more than double the nine-year average of 3.5%. Syndicates' predominantly fixed-income portfolios capitalized on the high interest rate environment that persisted through the year. However, SRL warns that this reliance on investment income could become a critical vulnerability. "Investment returns are likely to assume a greater significance in 2026 against a backdrop of (re)insurance price decreases and declining rate adequacy," the firm noted in its report.

This forecast is particularly salient as the economic landscape shifts. Central banks in key markets, including the U.S. Federal Reserve and the Bank of England, are widely expected to begin lowering policy rates in 2026. While fixed-income markets may still offer durable income, the era of rapidly appreciating returns driven by rising yields is likely over, placing renewed pressure on syndicates to generate profits from their core business of underwriting.

Softening Rates Signal a Turning Tide

The pressure on underwriting is already mounting as the reinsurance market enters a distinct softening phase. After several years of hard market conditions and steep price hikes, ample capacity and fierce competition are now driving rates down. The critical January 1, 2026, renewal season saw widespread price reductions, particularly in property-catastrophe lines, where some accounts saw rates fall by as much as 20%. This trend, driven by record-high global reinsurance capital estimated at over $760 billion, continued through the April renewals.

This pricing environment will inevitably squeeze underwriting margins across the market in the coming year. For the top-performing syndicates, the challenge will be to maintain discipline and leverage their expertise to select risks that can remain profitable in a less favorable pricing climate. For those already struggling, the softening market represents a significant additional headwind that could exacerbate their difficulties. The ability to navigate this downturn will be a true test of underwriting skill and strategic acumen.

The Gauntlet for Newcomers and the Future of Innovation

The "two-tier" dynamic and shifting market conditions create a particularly challenging environment for new and smaller syndicates. The fact that the bottom performers in a banner year were overwhelmingly recent startups raises questions about the barriers to entry and the sustainability of new ventures within the Lloyd's structure. These syndicates are now facing a softening rate environment just as they are trying to establish a foothold, having missed the peak of the hard market.

Despite these hurdles, the Lloyd's market is not static. Recent years have seen a trend of growth shifting toward small and mid-sized syndicates, suggesting an appetite for agility, niche expertise, and innovation. Furthermore, the market's strong performance has fueled active M&A, providing potential exit opportunities for successful ventures and a consolidation path for others.

Lloyd's itself is actively working to foster a more dynamic ecosystem, with a new five-year strategy focused on "focus, innovation and talent." Initiatives like the London Bridge 2 PCC structure are designed to attract new forms of risk capital, including from the insurance-linked securities (ILS) market. The ability of the next generation of syndicates to overcome the structural challenges and thrive in a more competitive landscape will be a crucial indicator of the market's long-term health and its capacity for renewal.