- Net Income Drop: $418.3 million in 2025, down from $587.5 million in 2024

- Total Assets Decline: $73.3 billion at year-end 2025, down from $106.9 billion in 2024

- Advances Plunge: Loans to members fell from $69.9 billion to $36.8 billion

Experts would likely conclude that FHLBank Pittsburgh's financial contraction reflects broader shifts in regional banking liquidity and Federal Reserve policy, though its commitment to community investment remains a key strength.

FHLBank Pittsburgh Profits Dip as Member Banks Shift Funding Strategy

PITTSBURGH, PA – February 19, 2026 – The Federal Home Loan Bank of Pittsburgh announced a significant drop in net income and total assets for 2025, a reflection of a broader shift in the regional banking landscape where member institutions reduced their reliance on wholesale funding. Despite the financial contraction, the bank reinforced its commitment to community development, exceeding its voluntary contribution targets for affordable housing and local initiatives.

The unaudited results paint a picture of a financial institution navigating a complex economic environment. Full-year net income for 2025 was $418.3 million, a marked decrease from $587.5 million in the prior year. This financial shift is indicative of larger trends reshaping the relationship between FHLBanks and the member institutions they serve.

A Story Told in Advances

At the heart of FHLBank Pittsburgh's financial results is a dramatic decline in advances—the loans it provides to its member banks, credit unions, and insurance companies. Total assets plummeted to $73.3 billion at the end of 2025, down from $106.9 billion just a year earlier. This contraction was driven almost entirely by a steep drop in advances, which fell from $69.9 billion to $36.8 billion.

According to the bank's release, this was the primary driver behind the decline in net interest income, which fell by $158.9 million to $625.1 million for the year. The bank cited "lower average advances and lower average short-term interest rates" as the main causes. This suggests a dual effect: member institutions were borrowing significantly less, and the loans that were made generated less income due to the prevailing interest rate environment.

The decline in demand for advances reflects a change in the liquidity management practices of the member institutions across Delaware, Pennsylvania, and West Virginia. As the press release notes, it is "not uncommon for fluctuations in advances to be driven by changes in member needs." In 2025, those needs clearly changed, pointing to a regional banking sector that was more liquid and less dependent on the FHLBank for day-to-day funding.

Monetary Policy and Member Liquidity

The story behind FHLBank Pittsburgh’s shrinking balance sheet is deeply intertwined with the Federal Reserve's actions and the resulting health of the regional banking sector in 2025. After a period of aggressive hikes, the Federal Reserve pivoted, cutting interest rates three times during the year. This easing of monetary policy, designed to support a weakening labor market, had a direct impact on bank funding strategies.

With lower short-term interest rates, the cost of alternative funding sources became more competitive. Simultaneously, many regional banks found themselves in a stronger liquidity position. Throughout 2025, the U.S. banking industry saw core deposits grow, partially fueled by a wave of mergers and acquisitions that consolidated assets within mid-sized banks. This provided many institutions with a larger internal pool of funds to support their operations and lending activities.

Furthermore, senior loan officers surveyed in early 2025 anticipated stronger loan demand throughout the year, driven by declining rates and increased spending needs. Armed with healthier deposit bases, many member banks were well-positioned to meet this demand using their own balance sheets rather than turning to FHLBank Pittsburgh for advances. This proactive management of liquidity demonstrates a strategic shift, where the FHLBank serves more as a crucial backstop for stability rather than a primary source of daily funding.

A Bellwether for the FHLBank System

The trends observed at FHLBank Pittsburgh are likely not isolated. As one of 11 such institutions across the country, its performance often serves as a bellwether for the entire Federal Home Loan Bank System. The macroeconomic forces at play—Federal Reserve policy, deposit trends, and member loan demand—are not confined to one region. It is highly probable that other FHLBanks experienced similar reductions in demand for advances as their member institutions also navigated this new liquidity landscape.

This system-wide contraction highlights the evolving role of the FHLBanks. Established during the Great Depression to ensure liquidity in the housing market, their importance fluctuates with the economic cycle. During times of market stress, demand for their advances surges. In periods of stability and ample liquidity, as was largely the case for many banks in 2025, their role shifts to that of a reliable, but less frequently used, partner.

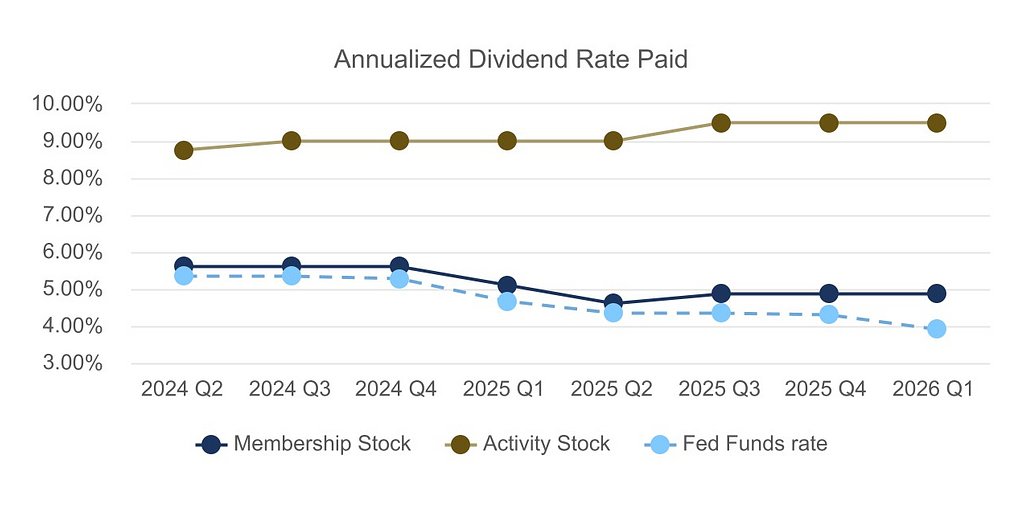

Despite the reduced borrowing, FHLBank Pittsburgh continued to provide significant value to its members. The board declared a fourth-quarter dividend of 9.50% annualized on activity stock and 4.85% on membership stock, delivering a meaningful return on investment to the institutions that capitalize the cooperative.

Community Investment Remains a Top Priority

While the financial metrics point to a year of contraction, FHLBank Pittsburgh's commitment to its community development mission grew stronger. In a clear demonstration of its dual mandate, the bank significantly exceeded its philanthropic goals for the year.

The bank's statutory Affordable Housing Program (AHP) assessment, based on a percentage of its earnings, was $46.6 million for 2025. These funds will be deployed in 2026 to support the creation and preservation of affordable housing across its district.

More notably, the bank's voluntary contributions to its suite of community products totaled an impressive $44.8 million, surpassing its commitment target of $35.3 million. These funds support a range of initiatives, including the Home4Good program for homelessness, the First Front Door program for first-time homebuyers, and the Blueprint Communities® revitalization initiative. On top of this, the bank made a supplemental voluntary contribution to AHP of $5.0 million.

This robust support, totaling over $90 million in combined statutory and voluntary community investments based on 2025 performance, underscores the institution's foundational purpose. Even as its own income declined, the bank prioritized and amplified its role as a key funding partner for projects that strengthen local communities, proving that its social impact is not merely an afterthought but a core component of its identity. This dedication provides a critical source of capital for non-profits and housing developers, particularly in an environment of economic uncertainty.

The results from 2025 show an institution adeptly balancing its responsibilities: providing reliable liquidity and shareholder returns to its members while simultaneously acting as a powerful engine for affordable housing and economic development in its region. While member demand for advances may ebb and flow with the economic tides, the bank's role as a pillar of both financial and community stability remains constant.

Topics & Related

International Relations

ESG

Interest Rates

Related Company Pulse