- New vehicle inventory down 20.7% quarter-over-quarter and 21.2% year-over-year

- Used commercial vehicle prices up 4.8% quarter-over-quarter and 6.3% year-over-year

- New vehicle sales dropped 25.8% quarter-over-quarter

Experts conclude that the commercial vehicle market is experiencing significant supply constraints due to tariffs and sourcing challenges, leading to higher costs and reduced availability for businesses.

Commercial Vehicle Market Squeezed by Tariffs, Q1 Data Reveals

CHICO, CA – May 19, 2026 – The nation's commercial vehicle market is experiencing a significant supply contraction, leaving businesses and fleet operators with fewer options and higher costs. A new Q1 2026 market analysis from Work Truck Solutions, a leading industry authority, reveals a sharp decline in new vehicle availability, a development directly linked to upstream sourcing challenges and new federal tariffs imposed late last year. The report paints a picture of a market under pressure, where a scarcity of new trucks is creating a ripple effect of rising prices and slowing sales in the used vehicle sector.

A Scarcity on the Lot: New Vehicle Inventory Plummets

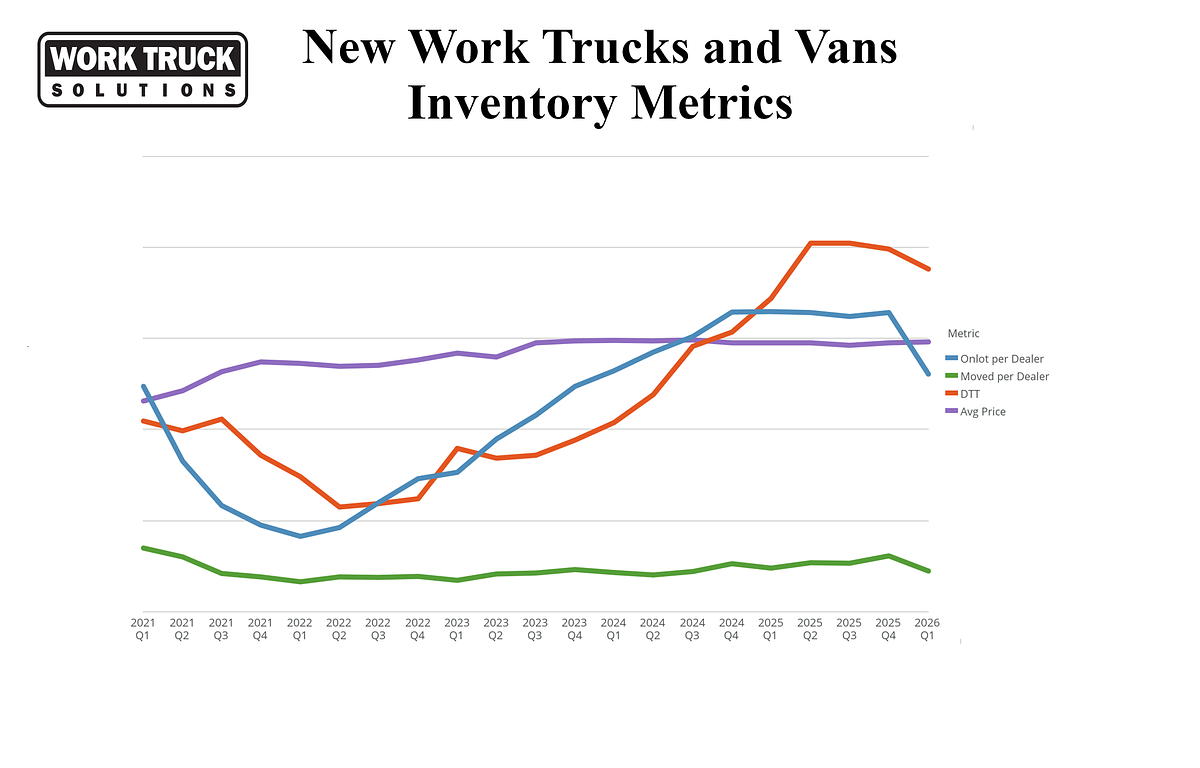

The most striking finding from the first quarter data is the dramatic tightening of new work truck and van inventory. According to the report, the average number of new vehicles on dealer lots plummeted by a staggering 20.7% compared to the previous quarter and fell 21.2% from the same period last year. This sudden scarcity has had an immediate and predictable impact on sales, which are constrained not by a lack of demand, but by a simple lack of available units.

New vehicle sales movement dropped 25.8% quarter-over-quarter. While prices for new trucks remained relatively stable, inching up just 0.4% to an average of $59,217, the underlying metrics tell a story of a market struggling to meet demand. The Days to Turn (DTT) for new vehicles—a measure of how long a vehicle sits on the lot before being sold—decreased by 5.5% from Q4 2025. This indicates that the limited inventory that is available is being snapped up quickly by buyers, further underscoring the supply-side nature of the crunch.

For businesses that rely on a steady flow of new vehicles to expand or refresh their fleets, from construction companies to last-mile delivery services, this shortage presents a significant operational hurdle. The inability to procure new, reliable assets can delay projects, increase maintenance costs on aging fleets, and ultimately hinder growth.

The Used Market Feels the Pressure

The shockwaves from the new vehicle shortage are now being felt acutely in the used commercial vehicle market. As fleet managers find it more difficult to acquire new trucks, they are holding onto their existing vehicles for longer. This has choked the flow of high-quality, low-mileage used trucks into the secondary market, creating a classic case of too much demand chasing too little supply.

Consequently, prices for used commercial vehicles have surged. The average final price for a used work truck or van climbed to $38,685 in the first quarter, a notable increase of 4.8% from the previous quarter and 6.3% year-over-year. Compounding the issue for buyers, the average mileage on these used vehicles also rose by 4.0% quarter-over-quarter, meaning businesses are paying more for trucks with more wear and tear.

Interestingly, despite the tight inventory and high demand, the turnover rate for used vehicles has slowed considerably. Days to Turn for used trucks increased by 12.7% to 62 days. This suggests a growing friction in the market, where elevated prices are causing buyers to become more cautious, potentially delaying purchasing decisions as they grapple with budget constraints and a limited, higher-mileage selection. This slowdown in sales, down 9.1% from the prior quarter, reflects a market where prices may be approaching a ceiling of affordability for many operators.

Behind the Numbers: The Impact of New Tariffs

The report from Work Truck Solutions attributes the market shift to “upstream cost and sourcing pressures, including those related to recent tariff activity.” Deeper analysis reveals this is not speculation. The market dynamics observed in Q1 2026 align directly with the implementation of significant trade policies enacted in late 2025.

On November 1, 2025, new tariffs resulting from a Section 232 national security investigation took effect, imposing a 25% duty on imported medium- and heavy-duty trucks and key components like engines, transmissions, and chassis. With U.S. government data showing that imports account for roughly 43% of all trucks sold in the U.S.—and up to 50% for heavy-duty Class 8 vehicles—the financial impact of this tariff was immediate and substantial for manufacturers and importers. These costs are now manifesting as reduced inventory flow and sourcing disruptions, as companies re-evaluate their supply chains and pricing structures.

The policy, designed to bolster domestic production, has in the short term created a bottleneck. The time lag between the imposition of tariffs and the potential ramp-up of domestic manufacturing capacity has left a void in the supply chain, which is now visible on dealership lots across the country.

An Uncertain Road Ahead: EVs and Market Adaptation

Even the burgeoning commercial battery electric vehicle (BEV) segment is not immune to the market’s complexities. While new commercial BEV sales showed robust year-over-year growth of 33.3%, they experienced a quarterly decline of 17.6%. This mixed performance, coupled with modest price increases, reflects a segment that is still finding its footing amid broader market volatility and evolving adoption patterns.

The current landscape presents a clear challenge to the entire commercial vehicle ecosystem. As Aaron Johnson, CEO of Work Truck Solutions, stated in the report, “The commercial vehicle market is clearly shifting. After a period of strong competition and healthy inventory levels in late 2025, we’re now seeing meaningful tightening.”

Johnson emphasized the proactive measures dealers and businesses must take. “Commercial dealers who stay proactive—leveraging digital merchandising, optimizing inventory visibility, and maintaining strong buyer engagement—will be best positioned to navigate whatever comes next.” For fleet operators, the path forward involves careful financial planning, a greater emphasis on vehicle maintenance to extend asset life, and exploring all available procurement channels in a market defined by scarcity and rising costs.

Topics & Related

Automotive

Geopolitics & Trade

Workforce & Talent

Revenue

Related Company Pulse