- 2025 Fintech Investment: US$2.4 billion across 113 deals, down from US$9.9 billion in 2024

- AI & Crypto Deals: 29 AI-focused deals and 26 cryptoasset/blockchain deals led investment priorities

- Open Banking Launch: Consumer-driven banking framework set to launch in 2026, enabling secure data sharing

Experts view the moderation in Canadian fintech investment as a sign of market maturation, with a shift toward sustainable growth, strategic technologies like AI, and regulatory clarity driving long-term value creation.

Canada's Fintech Reset: Maturity, Not Decline, Defines 2025 Market

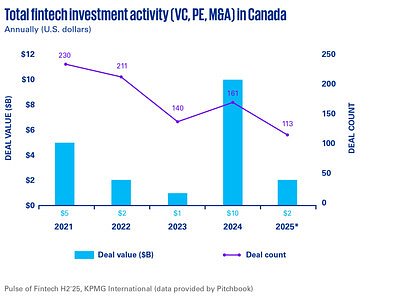

TORONTO, ON – February 18, 2026 – Canadian financial technology investment settled at a stable US$2.4 billion across 113 deals in 2025, a significant moderation from the previous year's record-breaking US$9.9 billion. However, a new report from KPMG suggests the drop in headline value signals not a decline, but a pivotal market maturation, as investors pivot from blockbuster megadeals to a more disciplined focus on sustainable, technology-driven growth.

The "Pulse of Fintech H2'25" report, using data from PitchBook, paints a picture of a sector shifting its priorities. The frenetic deal-making of the pandemic era has given way to a more discerning investment climate, where profitability, proven platforms, and strategic technologies like artificial intelligence and digital assets are now king.

A Tale of Two Years: Deconstructing the Moderation

To understand the state of Canadian fintech, one must look beyond the year-over-year comparison. The staggering US$9.9 billion invested in 2024 was largely an anomaly, inflated by two colossal transactions: the US$6.3 billion take-private deal of payments processor Nuvei and a US$1 billion private equity investment in travel tech firm Plusgrade. These two deals alone accounted for more than 70% of the year's total investment value.

When these outliers are excluded, the underlying investment in Canadian fintech during 2024 stood at approximately US$2.2 billion. Viewed through this lens, the US$2.4 billion raised in 2025 represents not a contraction, but steady, foundational growth. The market has returned to a more historical, and arguably more sustainable, level of activity.

This trend toward selectivity was particularly evident in the second half of 2025. While the number of deals declined, with 26 in Q3 and only 16 in Q4, the average deal size grew, reflecting a deliberate move by investors to write larger cheques for more established companies.

Dubie Cunningham, a partner in KPMG Canada's Banking and Capital Markets Practice, noted this shift in the report. "The investment appetite for Canadian fintechs will continue to grow in 2026, as investors prioritize quality, scale and strategic fit, signalling a market that is maturing and aligning more closely with long-term value creation," she says.

The year's largest transactions underscore this focus on maturity and scale. They included an US$898 million private equity buyout of IT solutions provider Converge Technology Solutions, Wealthsimple's US$536 million equity raise to fuel its expansive financial platform, and Ripple's strategic US$200 million acquisition of the stablecoin payments platform Rail.

The New Engines: AI and Digital Assets Take Center Stage

The story of 2025 was not just about how much was invested, but where it was invested. By deal volume, artificial intelligence and machine learning led the pack with 29 deals, closely followed by cryptoassets and blockchain with 26 deals. This concentration highlights a strategic pivot towards technologies that promise to fundamentally reshape financial services.

Investors are increasingly drawn to AI's potential to drive efficiency and innovation. "We're seeing a rapid acceleration of investor interest in AI-focused fintechs, driven by the sector's ability to unlock efficiencies and create new value through automation and advanced analytics," says Kareem Sadek, KPMG Canada's National Technology Risk Services Leader. "As financial institutions modernize their operating models, they're looking for scalable AI solutions that don't just streamline processes, but fundamentally reshape how decisions are made."

This confidence is bolstered by maturing regulatory guidance and stronger data governance practices, which Sadek notes will "accelerate investment in AI."

Simultaneously, the digital asset space is gaining institutional credibility. Regulatory developments, including the passage of the GENIUS Act in the U.S. and the Canadian federal government's move to create a clear regulatory regime for stablecoins, are providing the clarity investors have long sought. Sadek believes this will be a game-changer. "As Canada's new stablecoin regime starts taking shape in 2026, we expect a significant uptick in investor interest across the digital asset ecosystem," he adds. "With enhanced regulatory certainty, digital assets are positioned to become a bigger part of investors' fintech portfolios."

The Open Banking Catalyst

Looming on the horizon is perhaps the single most significant catalyst for the next wave of fintech innovation in Canada: the formal launch of the consumer-driven banking framework, or Open Banking, slated for this year. After years of consultation, the federal government is set to grant consumers the legal right to securely share their financial data with accredited third-party providers.

Oversight of the framework will fall to the Bank of Canada, which will manage a phased rollout. The first phase, expected in early 2026, will enable "read-only" access, allowing consumers to aggregate their account information across different institutions. A second phase, planned for mid-2027, will introduce "write access," enabling functions like payment initiation and seamless account switching.

This shift from insecure "screen scraping" to secure, API-based data sharing is expected to dismantle long-standing barriers to competition. It will empower a new generation of fintech applications for budgeting, financial planning, and product comparison, ultimately giving consumers more choice and control.

Challenger Banks Poised for Momentum

No segment is better positioned to capitalize on Open Banking than Canada's burgeoning challenger banks. Firms like EQ Bank, Neo Financial, and Koho have already made inroads by offering digital-first, user-friendly alternatives to traditional banking. The new framework promises to supercharge their growth.

As noted by KPMG's Dubie Cunningham, the challenger bank market is an area she is keeping a close eye on. "Canada's challenger bank market is poised for momentum in 2026 as newer entrants launch more competitive products, improve customer experiences and strike new partnerships," she states in the report. "The roll out of Canada's open banking framework – expected this year – will also serve as a catalyst for more investment in the sector."

By enabling secure data portability, Open Banking will make it easier for customers to switch to providers that offer better rates, lower fees, and more personalized services. This could fundamentally alter the competitive landscape, turning incumbent banks into back-end infrastructure providers while nimble fintechs win the battle for the customer interface. As the framework comes online, the disciplined investment of 2025 may look like the quiet foundation for a much more dynamic and competitive financial ecosystem in the years to come.

Topics & Related

AI & Software Platforms

AI & Machine Learning

Fintech

Machine Learning

Trade Wars & Tariffs

Policy Change

Acquisition

Related Company Pulse